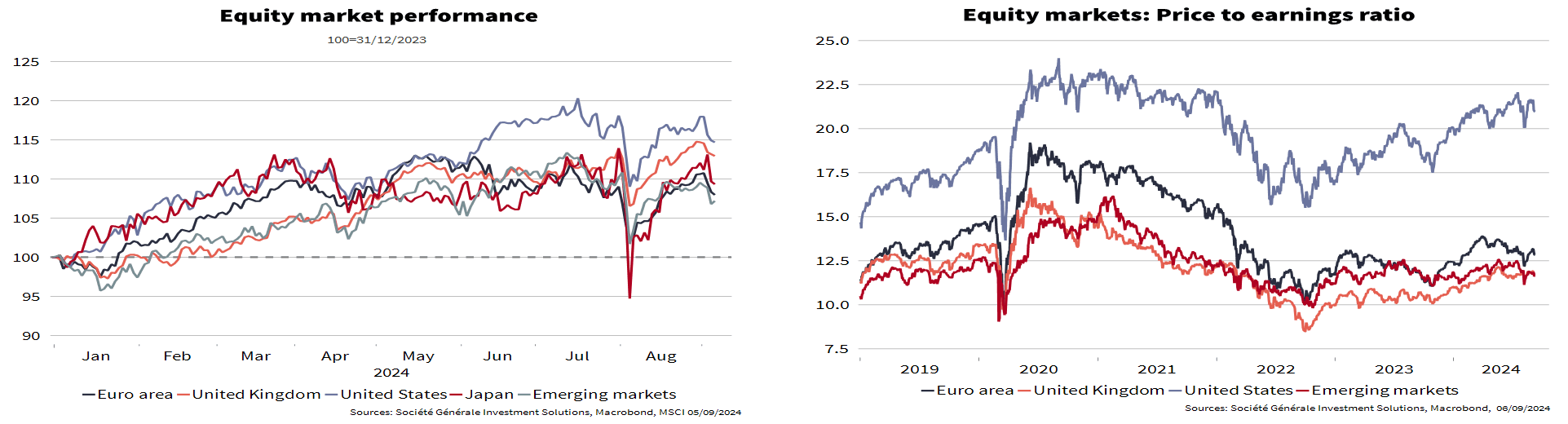

US. After more than a year of outperformance, US equity markets slipped back in the summer, falling -2.9% since mid-July compared to -2% for global markets. Tech and growth stocks went into the summer as the biggest gainers year-on-year, but they not only fell hardest during the slump but recovered least during the rebound. Partly this reflected the mixed data coming out of the US economy – although in our view the figures continue to point to a soft landing. Given the high multiples on which the market is trading and its vulnerability to economic news, we decided to move to a more neutral view on US equities. That said, US companies are still growing earnings and the economy is proving pretty resilient. Fed rate cuts coupled with a soft landing for the economy could also help buoy markets. We have therefore moved from Overweight to Neutral on the United States, with no preference on style.

Euro zone. European equities also had a hard summer and have not yet recovered to their mid-July levels. But they still held up better than the global market average. Despite the weak economy and political uncertainty, we remain Overweight euro zone markets, which remain attractively valued in absolute terms. Also, impending rate cuts by the ECB and falling inflation should help sustain consumer spending, which has been feeble since the Ukraine war broke out. Another potential plus point for the European market is its large exposure to value stocks, which seem to be enjoying healthy momentum since the summer.

UK. The UK market has rallied strongly by +2.2% since mid-July, helped by a heavy bias toward defensive stocks which had a good summer. But it still lags global markets year-to-date and year-on-year. Looking ahead, though, the market has several benefits: pricing looks cheap, the Bank of England began cutting rates in August and there are even some modest signs the economy may be picking up. We therefore stand by our Overweight to this market.

Japan. The Japanese stock market went into the summer as one of the top-performers year-on-year and came out as the season's biggest loser, down -9.6%, not helped by narrowing rate spreads to the United States and a yen rally. The market has some bull factors: reforms to corporate governance, high corporate earnings and the end of deflation accompanied by a gradual exit from the zero-rate policy. And some bear factors, including a volatile yen and heavy bias toward technology and communications stocks. We remain Neutral.