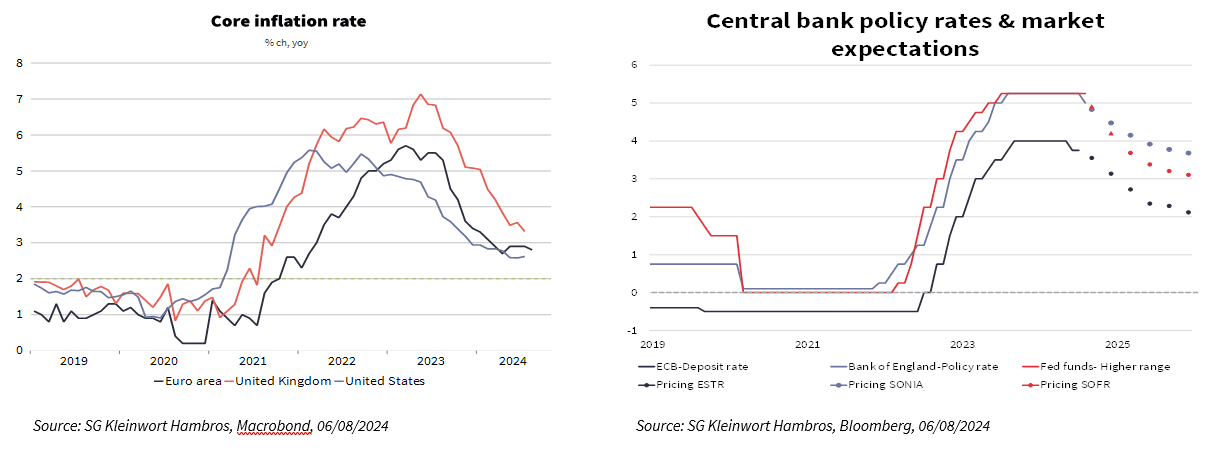

The ECB needs to watch Germany's weak economy. In Europe, the German economy continues to show signs of weakness. It has proven especially vulnerable to three recent shocks: Covid, the Ukraine war and the slump in the Chinese economy. Germany makes up a third of the euro area economy and a sluggish Germany automatically drags down the region’s growth. With inflation apparently under control at long last (+2.2% year-over-year in August), the European Central Bank (ECB) could be tempted to loosen monetary policy faster to help the German economy and give the wider European economy a boost. At the moment, markets are discounting two rate cuts this year and six by next September. If current indicators on the economy and inflation are confirmed, it might want to go harder and faster, with three cuts this year. The Bank of England opted to cut rates in August and could do so again in November when it publishes its new economic forecasts. UK inflation is back near target (+2.2% year-over-year in July) and likely to hover around this level for the next few months, raising the possibility of another rate cut in December.

Bank of Japan (BoJ) bucks the trend. The Bank of Japan sprung a surprise rate hike on markets in late July and looks set to continue its tightening cycle. Inflation now looks to have peaked. Headline inflation was unchanged at +2.8% year-over-year in July and underlying inflation fell slightly to +1.6%. Japan's long struggle with deflation now seems to be over. This should encourage the BoJ to continue moving toward a more conventional monetary policy. The People's Bank of China has sought to revive moribund domestic demand by repeatedly cutting rates and pumping liquidity into banks. Further cuts, more closely targeted on the property market, may be announced in coming months.