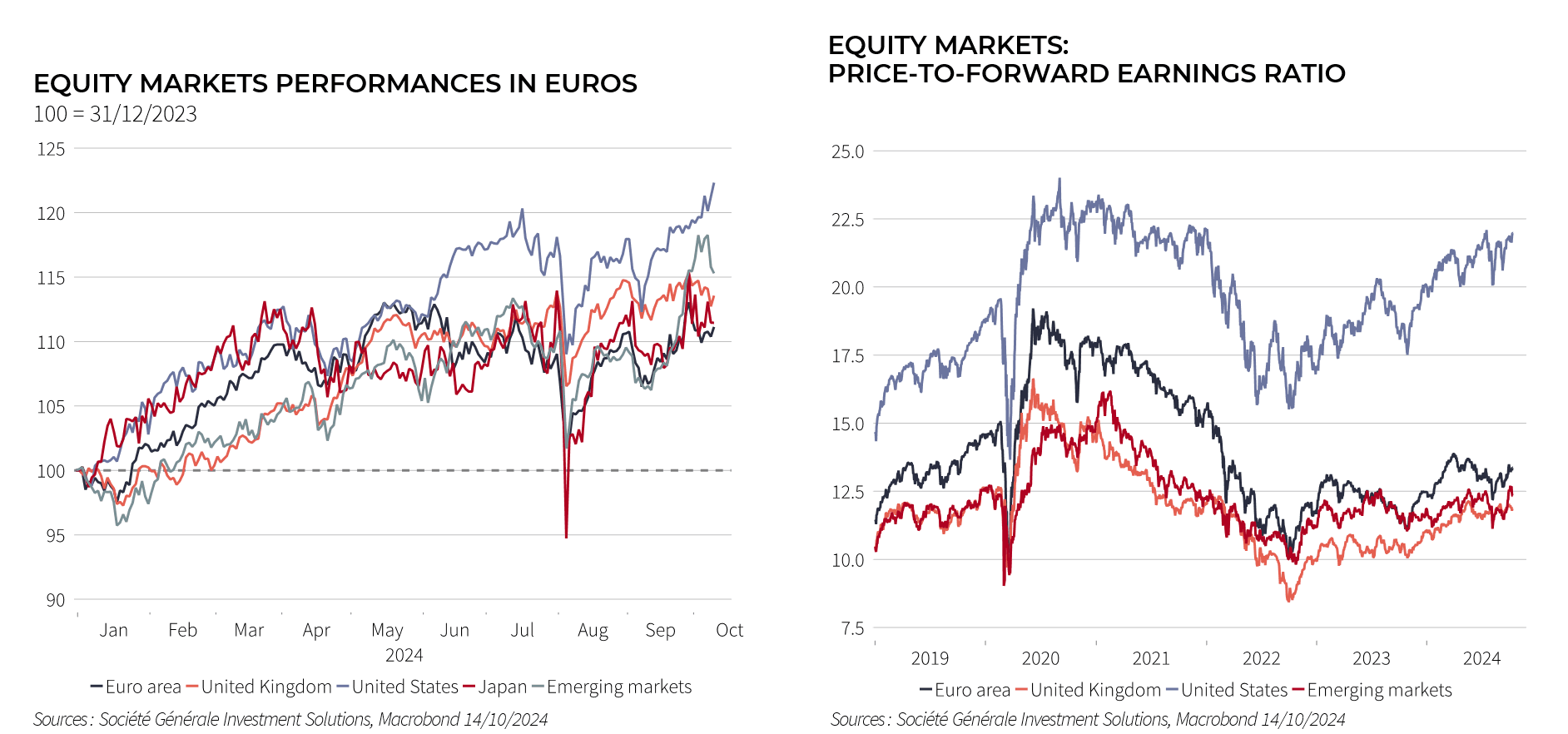

US. US stock market performance since the start of Q3 was broadly in line with the global index (up 6.2% each), despite the summer’s large correction. However, there has been some rotation in investor preferences for style and market cap: value stocks and small caps have substantially outperformed. This broadening of performance, coupled with a robust economy and Fed rate cuts, should be good for US equity markets. What is more, company profits are on the rise, whether measured at macro-level (in the national accounts) or micro-level (earnings). However, the United States market looks expensive whether in absolute terms (P/E) or relative to government debt (equity risk premium). Further, the presidential and legislative elections scheduled for 5 November could lead to a difficult and uncertain political outcome, likely to foster more volatility.

Euro Area. European equities have substantially underperformed since the start of Q3, gaining only 1.9%, held back by economic problems, notably in Germany, political uncertainty in France and lacklustre corporate earnings. We nonetheless remain Overweight on these markets, which are still cheap in absolute terms. Moreover, while earnings growth may be on a downtrend, profit margins remain historically high and net debt (debt minus bank deposits) is back to the levels not seen before the financial crisis. Finally, although growth is set to stall briefly in late 2024, it should bounce back in 2025.

UK. Like the euro area, UK equity markets underperformed the global index since Q3, putting on 1.9%. However, we are keeping our Overweight to this market which remains one of the cheapest on offer. Falling interest rates and the return of some political stability should also be good for UK stocks. The London market has a high share of value stocks, and this could also prove helpful in a context of equity market style rotation.

Japan. Having strongly outperformed the global market until mid-2024, the Japanese market has since fallen by 1.7%. A volatile yen, monetary policy that runs counter to the other main central banks and the heavy weighting of growth stocks seem to have turned investors against Japanese equities. Even so, we prefer to remain at Neutral on this market.