Europe is heading for a temporary soft-patch. The euro area economy is looking less healthy. Germany's industrial output continues to be hampered by high energy costs, weaker demand from China, Chinese competition especially in the auto sector, and stagnant household consumption. In France, now that the Olympics bump has faded, sentiment among households and companies seems to be depressed by the political uncertainty prevailing in the country. The upcoming fiscal policy tightening could also weigh on growth. The wider euro area economy thus looks set to slow towards the end of the year, but the slowdown will likely be short and shallow. Countries such as Italy and Spain remain on a stronger growth trend. The region may benefit from a simultaneous retreat of inflation – down from 2.2% year-over-year in August to 1.8% in September – and easing of European Central Bank (ECB) rates. Markets are pricing in 50 bp of further cuts by the turn of the year and 100 bp in 2025. Nevertheless, the stuttering economy could prompt the ECB to bring rates down faster.

In the United Kingdom, the economy seems to have held up better than in the euro area. As inflation, particularly in services, is proving sticky, the Bank of England looks to be treading a more cautious line than its peers. That said, the government is set to announce a fiscal squeeze and this, coupled with a strong pound, could lead the Bank of England to make two rate cuts this year.

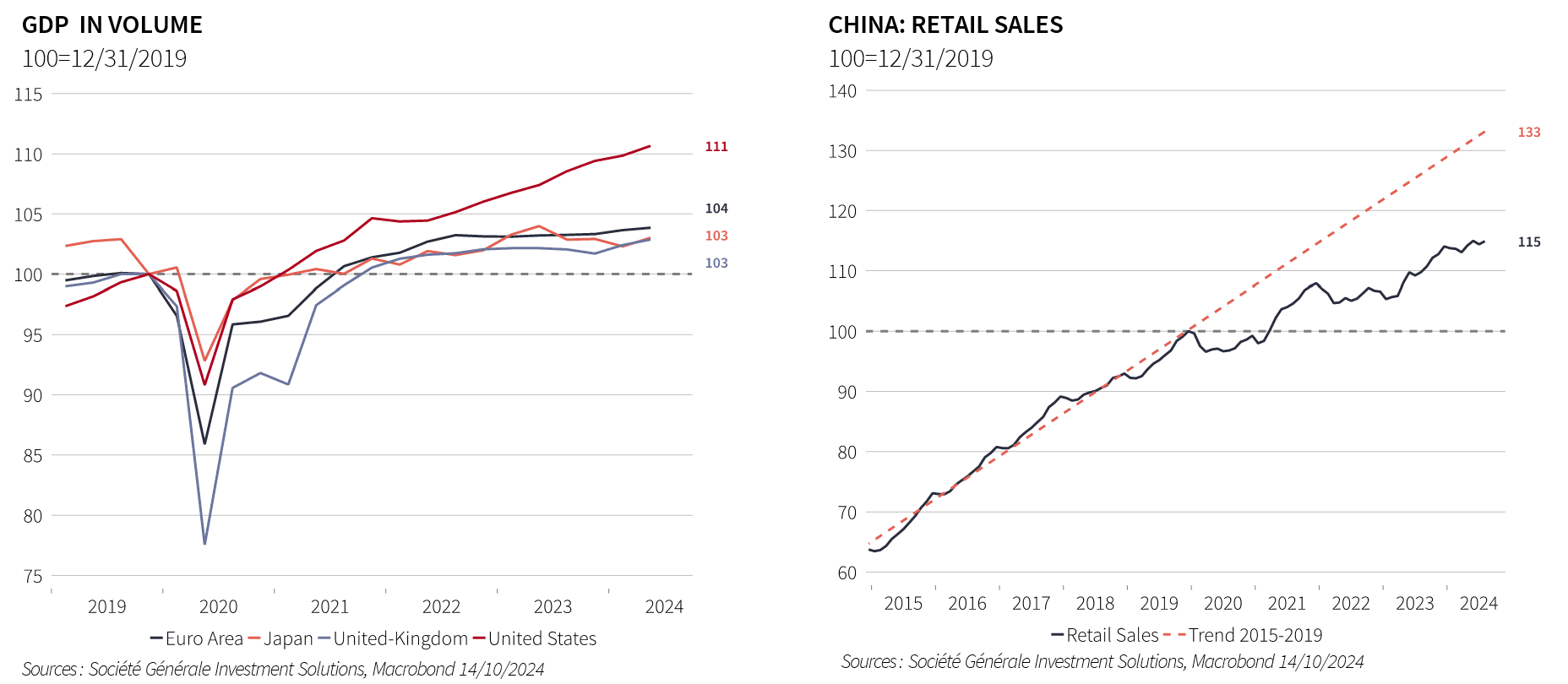

In China, the economy still seems to be mainly powered by industrial production and exports. Consumption remains muted, with households still negatively impacted by property market woes. In response, Chinese authorities have announced a far-reaching package of measures to revive the economy. As a first step, China's central bank (the PBoC) announced rate cuts and macro-prudential measures. This was followed by a commitment at the recent Politburo meeting to deploy “necessary fiscal spending”. This was welcome news to markets, but the details of the measures and their likely long-term impact remain uncertain.