Click the links to jump to a section, or flip the page to read all.

CURRENCIES

We remain Neutral on equity markets, with a clear preference for European regions over the US, given its better momentum and profit outlook.

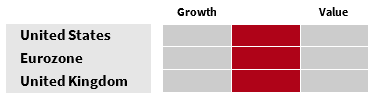

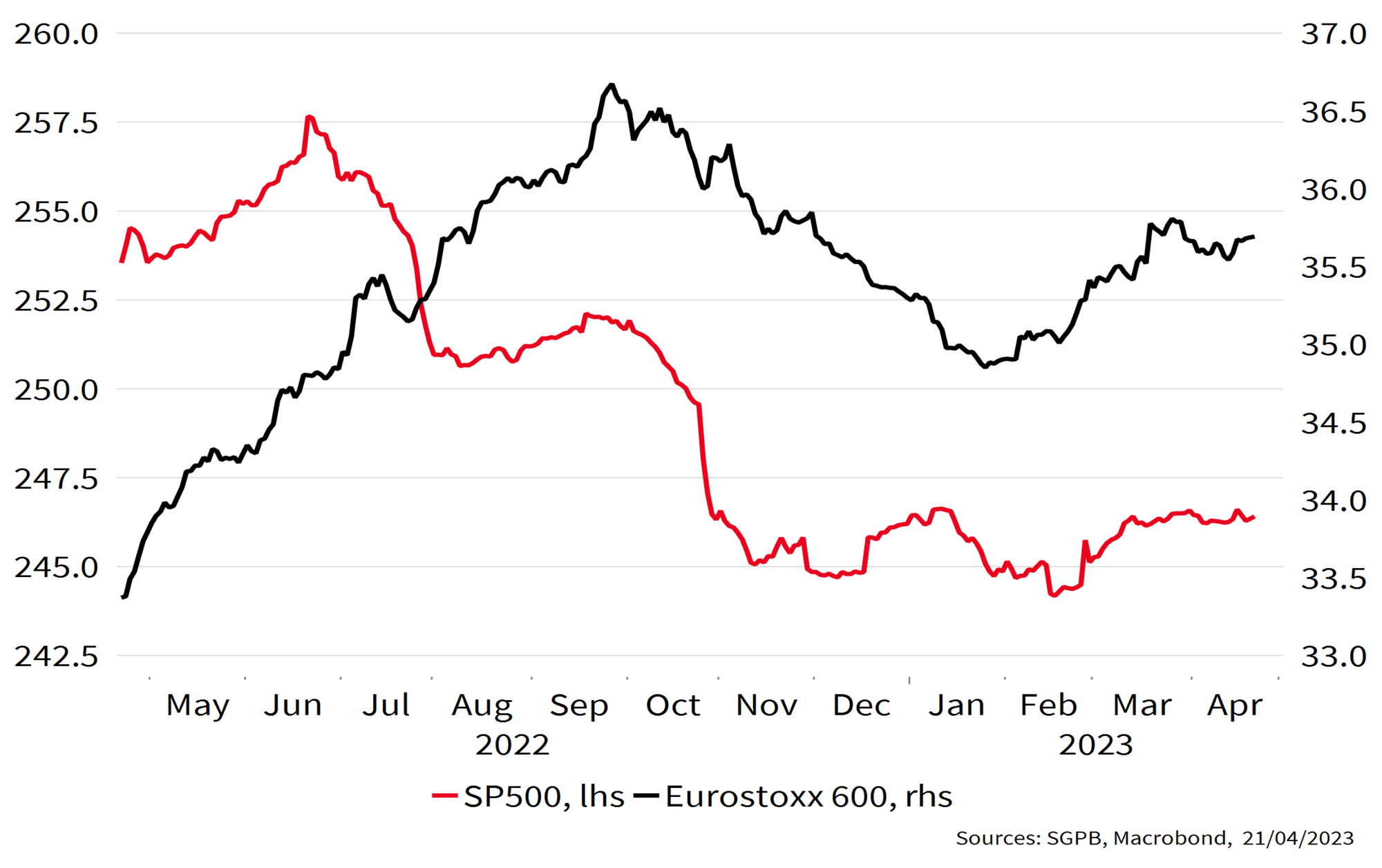

US. US equity markets have registered a substantial bounce back since the bankruptcy of SVB triggered concerns for the international banking system. The S&P 500 is up 7% since mid-March and the Nasdaq 100 rallied 10% over the same period. The rally owes much to receding fears of a systemic crisis after the authorities took steps to ease the pressure on regional banks’ sources of funding. Also, expectations of a credit squeeze and economic slowdown led some to price in Fed rate cuts for H2 2023, further encouraging the rally. However, we think growth will remain modest over coming months and underlying inflation will persist, persuading the Fed to hold its policy rate at 5% all year. Also, corporate earnings seem to be on a weakening trend, having fallen since Q3 2022, with 2023 guidance remaining sluggish. Overall, we continue to Underweight US equities.

UK. The FTSE 100 has also put on 8% since the banking wobble. UK companies are reporting strong profit growth in an environment where the sector biases of the UK stock market (such as commodities and health) play well. We remain Overweight UK equities.

Europe. As in the United States, European stock markets have boomed since the onset of banking concerns and the rescue of Crédit Suisse. The region’s main equity index Euro Stoxx 50 is up 8% since the flurry of banking tensions, outshining their US equivalents since Q4 2022. This strong performance primarily reflects the improving economic outlook as energy risks have waned and China's economy has reopened. Corporate profits grew strongly in 2022 and earnings guidance remains bullish. Finally, despite the recent rally, valuations of European indices remain attractive, with a forward price to earnings ratio close to its long-term average. Accordingly, we retain a higher exposure to the European market.

Japan. The Japanese economy remains the only one amongst its peers where persistent inflation is viewed positively: after decades of deflation, companies may well benefit from the opportunity to raise prices. However, the Bank of Japan’s pivot to a more hawkish policy stance lags way behind its Western counterparts, keeping pressure on the Yen for the time being. We are Underweight.

Emerging markets. The revival of the Chinese economy, including household consumption, should boost company revenues. Other major emerging economies should also be able to benefit from China’s accelerating growth. We remain Neutral.

Style Preference

Earnings per share expectations for the next 12 months

Past performance does not prejudge future performance. Investments may be subject to market fluctuations, and the price and value of investments and the resulting revenues may fluctuate downward and upward. Your capital is not protected, and original investments may not be recovered.

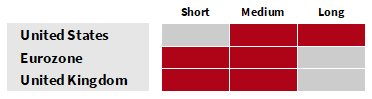

Bond markets now seem to have priced in most of central banks’ policy tightening and yields are attractive, even in real terms. We remain Neutral on sovereign debt with a preference for the shorter end of the curve, and Underweight Credit for the time being.

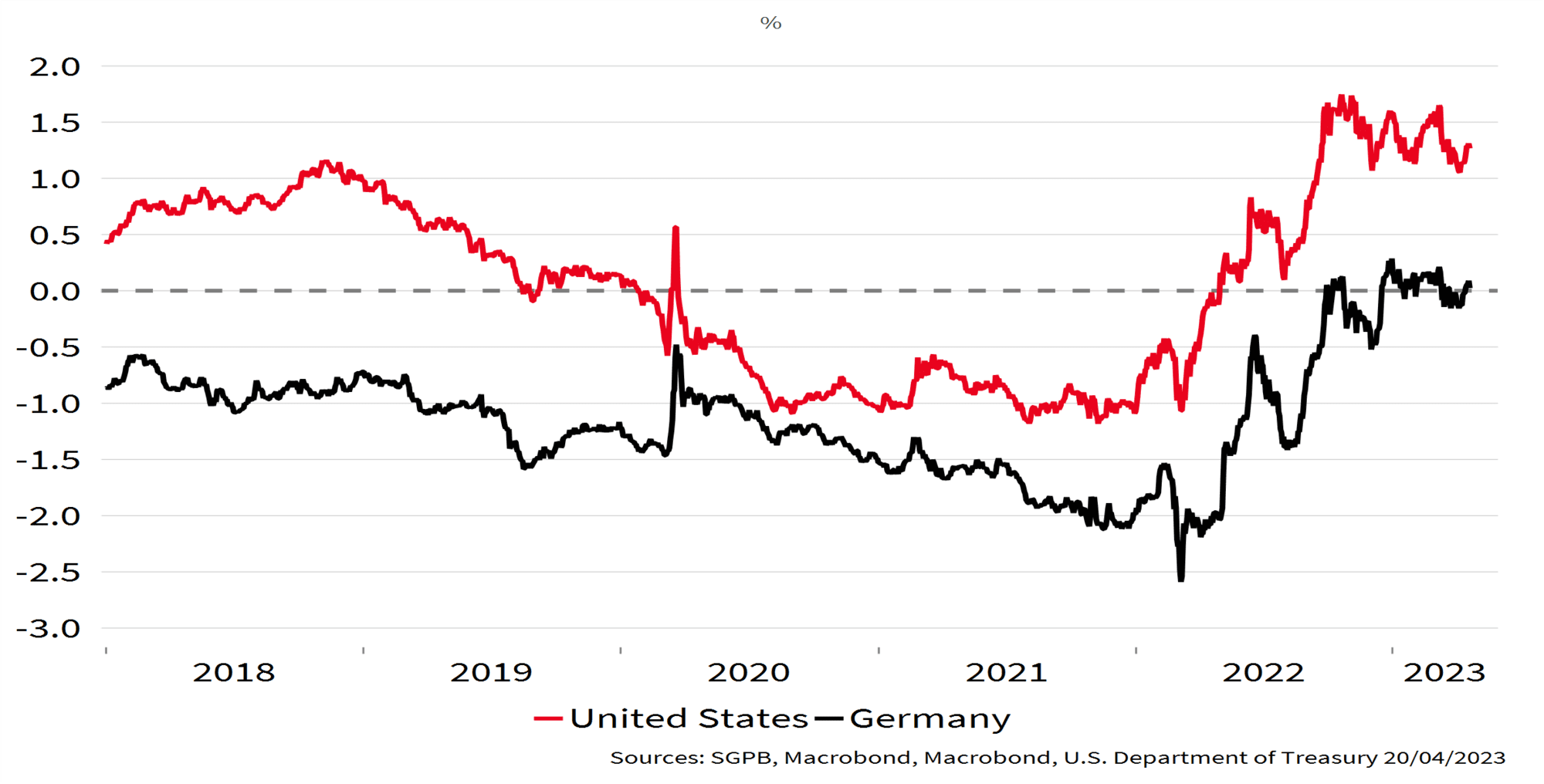

US. Treasury yields have been trending upwards since the end of the banking turbulence. Yields on the 10-year T-bond had dipped to 3.30% before a 30 bps rally took them back to 3.60% recently, mainly thanks to resilient economic numbers. Job creation figures confirm the labour market is holding up well. Inflation-wise, headline figures continue to drop, to 5% in March from 6% in February, but the core measure ticked up to 5.6% in March, from 5.5% the previous month.

However, household consumption is starting to show signs of slowing down. The Fed is likely to further tighten policy with a quarter-point rate hike at its next meeting, but then keep rates on hold until underlying inflation is well below current levels. It will also be keeping a close eye on fallout from the recent banking wobble and how tight financing conditions get in coming months. Overall, we remain Overweight Treasuries which are paying attractive returns, including positive real yields.

Duration Preference

UK. Gilt yields also rose, with the 10-year bond topping 3.8% and the 2-year bill 4.3%. Inflationary pressures are persistently high, although should fall significantly at the headline level as the base effects of surging energy prices one year ago begin to dissipate. Core inflation remains troubling amid ongoing strong wage pressures. The Bank of England's challenge is to get inflation back toward its target without toppling a still fragile economy and is likely to opt for further monetary tightening, with a 25 bps hike at its next meeting. This context keeps us Neutral on Gilts.

Eurozone. Yields on Euro area sovereign bonds have also been on an uptrend, boosted by resilient economic data. This suggests that monetary tightening will continue for the time being. The 10-year Bund and OAT rates have increased to 2.5% and 3%, respectively. The economy continues to hold up well, with PMIs surprising on the upside as both headline and core inflation continue running too high at 6.9% and 5.7%, respectively. Labour markets are still dynamic, stoking wage pressures. Looking at this environment, the ECB is likely to stick to its hawkish tone. Its key priority is to get inflation back near 2% compatible trend, suggesting a 25 bps rate hike at its next meeting. That said, the trend in the distribution of bank lending will remain a core focus. Overall, we remain Neutral on European sovereign debt.

Developed markets. We remain Underweight investment-grade and high-yield corporate debt, given the pressures on financing as well as continuing risks of an economic slowdown that could hit riskier firms hardest.

Real 10-Year Bond Yields

Past performance does not prejudge future performance. Investments may be subject to market fluctuations, and the price and value of investments and the resulting revenues may fluctuate downward and upward. Your capital is not protected, and original investments may not be recovered. Duration: short = Up to 5 years, medium = 5-7 years, long = 7+ years.

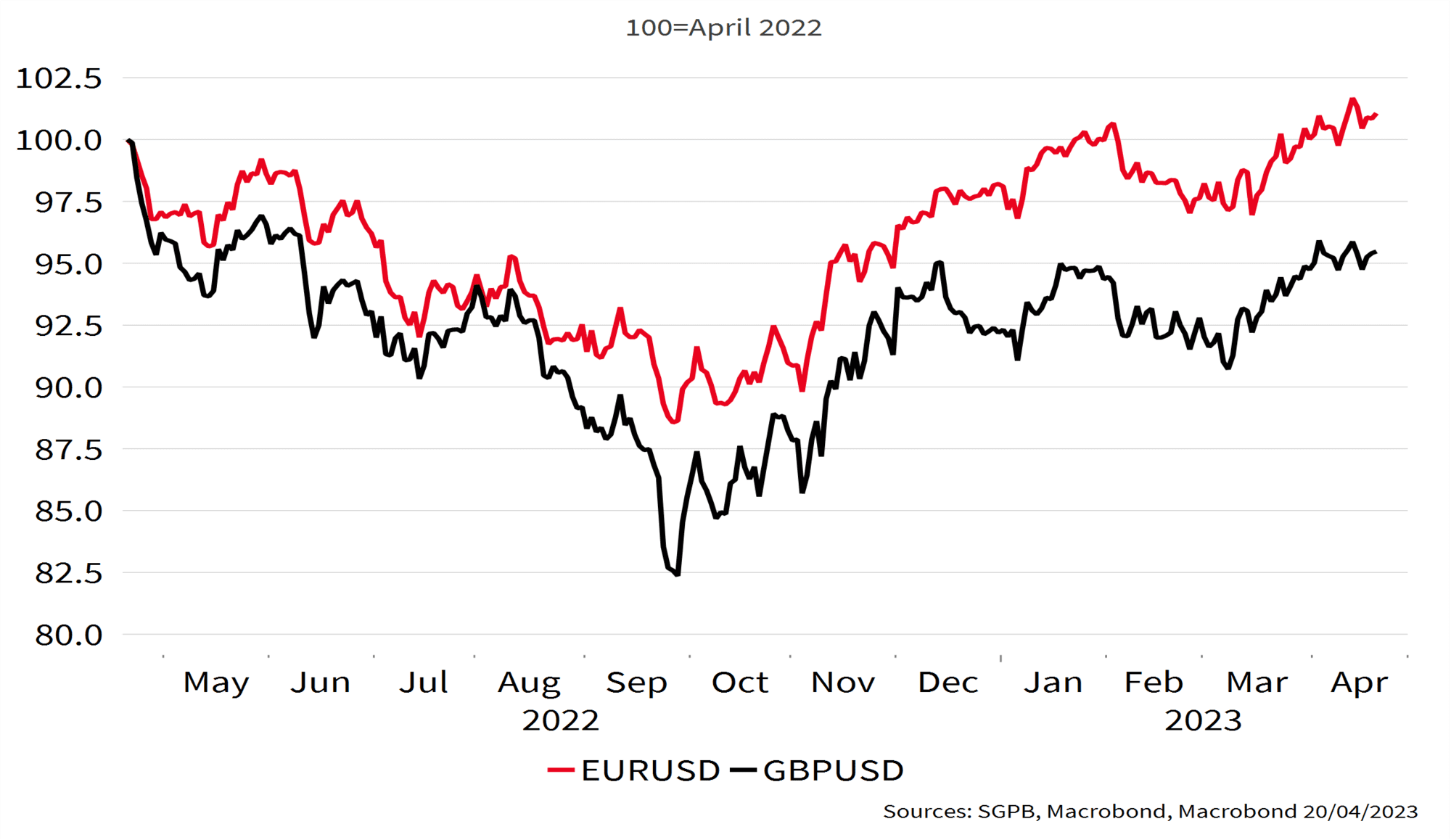

Receding fears for the banking systems of developed economies meant the dollar lost ground in its main crosses. The narrowing gap between Fed and ECB/BoE rates means we continue to prefer the EUR and GBP.

Dollar Index. The US dollar lost ground in its key crosses with developed and emerging market currencies. Among emerging currencies, the big winners were the Mexican Peso, Chilean Peso and Brazilian Real, up by an average 3.5% vs. the dollar on the month, as fears of a possible banking crisis receded, and all three countries posted improved balance of payments figures. The Fed looks set to put rates on hold at its upcoming May meeting, containing any dollar upside for the next few months.

GBP/USD. We remain Overweight sterling against the US dollar. The pound edged up 1.5% against the dollar over the month on the prospects for interest rates. This trend should persist in coming weeks with external pressures easing given lower perceived political risks and a better balance of trade, and the Bank of England braced to continue tightening monetary policy.

EUR/USD. We also remain Overweight the euro against the dollar. The single currency rose 2.5% over the last month as banking concerns eased. Nevertheless, we think the euro has further to climb against the dollar as the gap between Fed and ECB rates should continue to narrow and Europe's balance of payments figures should continue to improve.

JPY/USD. The Japanese currency lost 2.4% against the dollar as the rate gap between the two currencies widened. Japan is, for now, sticking by its yield curve control system, in which the Bank of Japan caps the 10-year government bond yield at 0.5%. Markets expect the new governor, Mr Kazuo Ueda, to gradually exit the yield curve control system because Japanese inflation has finally passed the 2% threshold, nominal wages are also starting to rise faster than 2% and the system forces the BoJ to keep buying sovereign bonds even though it already holds over 40% of the total outstanding. We are Overweight.

EUR and GBP vs USD exchange rates

Emerging market currencies. China’s sustained efforts to promote the use of the renminbi and end the dominance of the US dollar in the global financial system was strengthened this month as Brazil’s president Luiz Inácio Lula da Silva called on developing countries to replace the dollar with their own currencies in international trade. The determination to challenge the dollar cannot be underestimated as emerging economies including China, India and Russia are in discussion with Brazil and South Africa about the formation of a new currency. Whilst this may generate concerns among currency investors, the sizable challenge of fulfilling this ambition means most transactions are expected to remain in dollars for now. We are Neutral.

We maintain our Neutral position on commodities generally, and gold continues to play its full role as a safe haven asset. Hedge Funds may have lost some of their shine compared to the protective benefits of yield-bearing fixed income products, yet they remain a core pillar of our diversification strategy.

Commodities. We maintain our neutral position on industrial commodities. The price per barrel of oil is under pressure and this situation is likely to persist due to concerns about declining demand, despite a better-than-expected economic recovery in China. To safeguard its pricing power, OPEC recently announced a surprise production cut that resulted in a temporary bounce in oil prices, which has since dissipated.

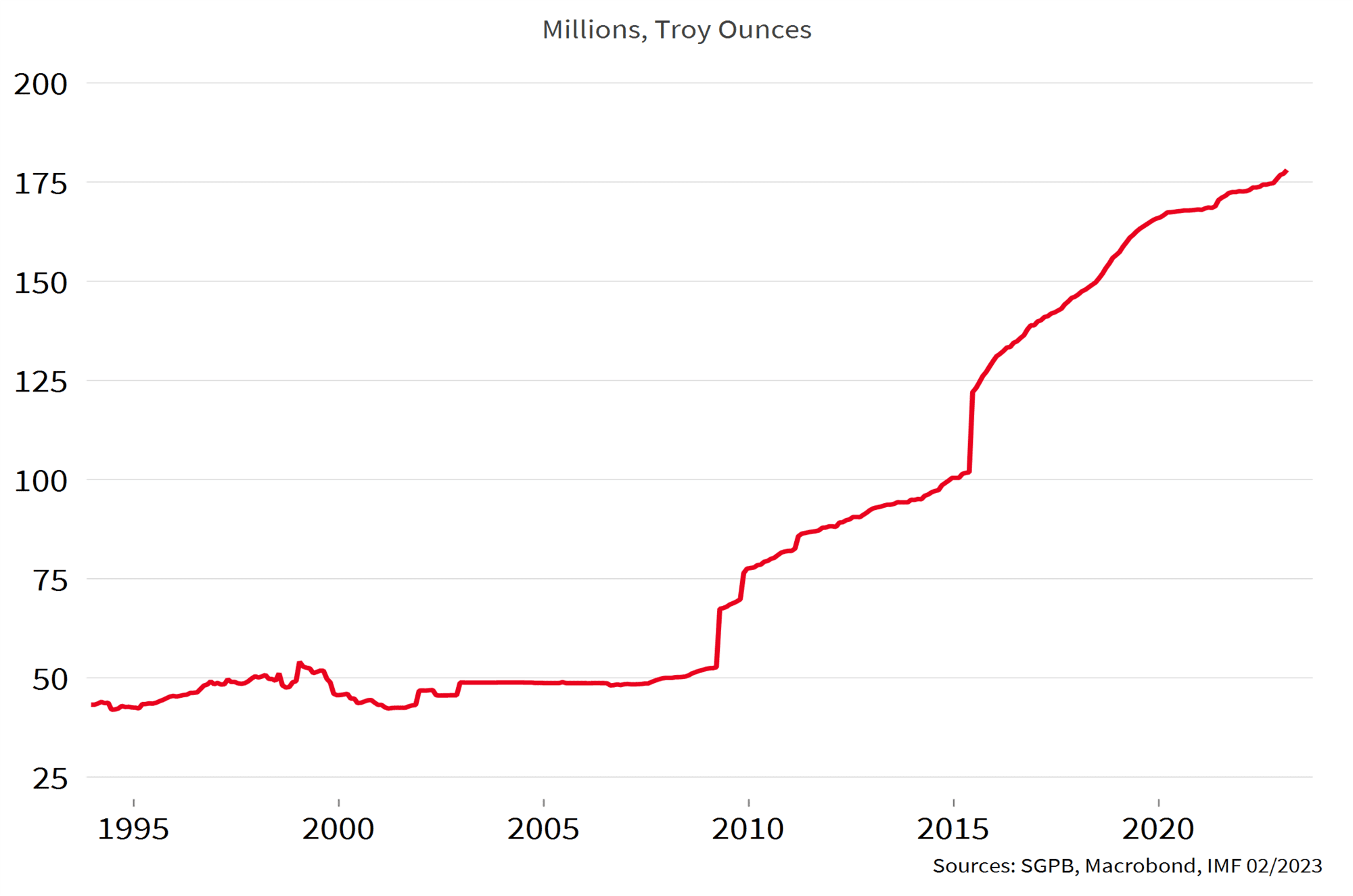

Gold. We remain overweight gold, primarily because of its safe-haven status. Although the financial backdrop is favourable, with easing banking tensions, a falling dollar and falling bond yields, the trend for the gold price is upwards. This illustrates both investor caution and continued buying by central banks.

Main Emerging Markets: Central Bank gold holdings

Infrastructure & specialist property. We hold an allocation to a diversified portfolio of infrastructure (such as energy storage and efficiency, smart grids, waste-to-energy, air treatment and digital infrastructure) and specialist property assets (including care homes and e-commerce and logistics warehouses). These real assets offer additional diversification from other risk assets such as equities, as well as an attractive income stream and reasonable sensitivity to inflation.

Hedge Funds. In unstable market conditions hedge funds can help a portfolio, but selectivity is key. We prefer strategies which hold their own in bear markets, such as Merger Arbitrage, trend followers and Equity long/short. These strategies provide relatively safe, uncorrelated sources of returns from equities. Our hedge funds allocation has performed well over 2022 and have been a great diversifier in our strategies.

Tail Risk Protection Note. Tail risks are typically understood as unlikely but severe crisis events which shock markets and dramatically impact the value of risk assets negatively. The dot-com bust at the turn of the century and the Great Financial Crisis in 2008 and 2009 are examples of such events. Despite conditions not being favourable for it in 2022, we believe the Tail Risk Protection Note offers our portfolios yet another critical source of safety and complements the existing diversifiers.