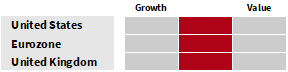

US. We are moving from Underweight to Neutral on US equities. The US economy has proven its resilience since the start of the year despite some significant headwinds, such as bank failures and debt ceiling discussions. GDP grew 1.3% (year-on-year) in Q1 2023 and, based on purchasing managing surveys, should stay on the right path in H2. Falls in headline inflation open up the prospect of household incomes growing in real terms, supporting the outlook for resilient household consumption. What is more, surplus savings accrued during Covid remain close to 4% of GDP (compared to a peak of 10% in 2021) and continue to bankroll household spending. On the corporate side, companies are awash with cash and, while margins are coming back down toward pre-Covid levels, they remain attractive. We prefer a balanced mix of Growth and Value stocks, and we are positioning portfolios for a broader market recovery.