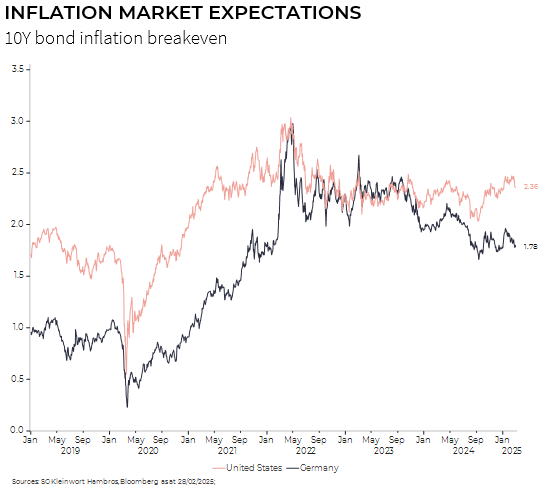

While inflation has fallen in 2024 in the main developed economies, it is once again showing signs of nervousness in the United States. There are two explanations for these tensions: still robust activity and fears about the inflationary effects of the new administration's measures. The Federal Reserve will likely wait for inflation expectations to moderate before changing its monetary policy. In Europe, on the other hand, inflation expectations remain well anchored and would allow central banks to continue easing their key rates.

First half of the year likely to be a continuation of 2024. The divergences observed in economic growth in 2024 should continue, at least during the first half of 2025. In the United States, the economy should continue to benefit from solid fundamentals (corporate profit margins elevated, healthy household balance sheets and high productivity gains). In the euro area, after flirting with recession at the end of 2024, growth is likely to remain marginally positive in the first half of the year. Nevertheless, the fall in inflation and the cut in key interest rates should encourage consumers to save less. Finally, in China, the difficulties in the property market are likely to persist, continuing to weigh on household consumption (real-estate being the households’ main asset) and therefore on the Chinese economy.

The second half of the year will depend on the direction of economic policy. After a busy electoral year in 2024, 2025 will be marked by the economic policy decisions of the new governments. The transition from campaign promises to their implementation is producing a great deal of uncertainty about both growth and inflation in the major economic areas.

United States: the risk of a return to inflation. The key source of uncertainty comes from the United States, with implications for the rest of the world. The timing, geographical reach and scale of any rises in US tariffs remain unknown. The same goes for migration policy. These two measures could potentially prompt a resurgence in US inflation, particularly with the US labour market still tight, and could also damage growth in targeted countries with a blowback impact on US growth if these countries retaliate.