Despite the high valuation levels, the high concentration of performance in a few companies, and the inflationary risks posed by trade policy, we keep a positive view on this market. We favour sectors and styles that would benefit from favourable industrial policy and that would withstand the higher interest rate environment, in particular value stocks, mid-caps, and sectors such as manufacturing, finance, and healthcare.

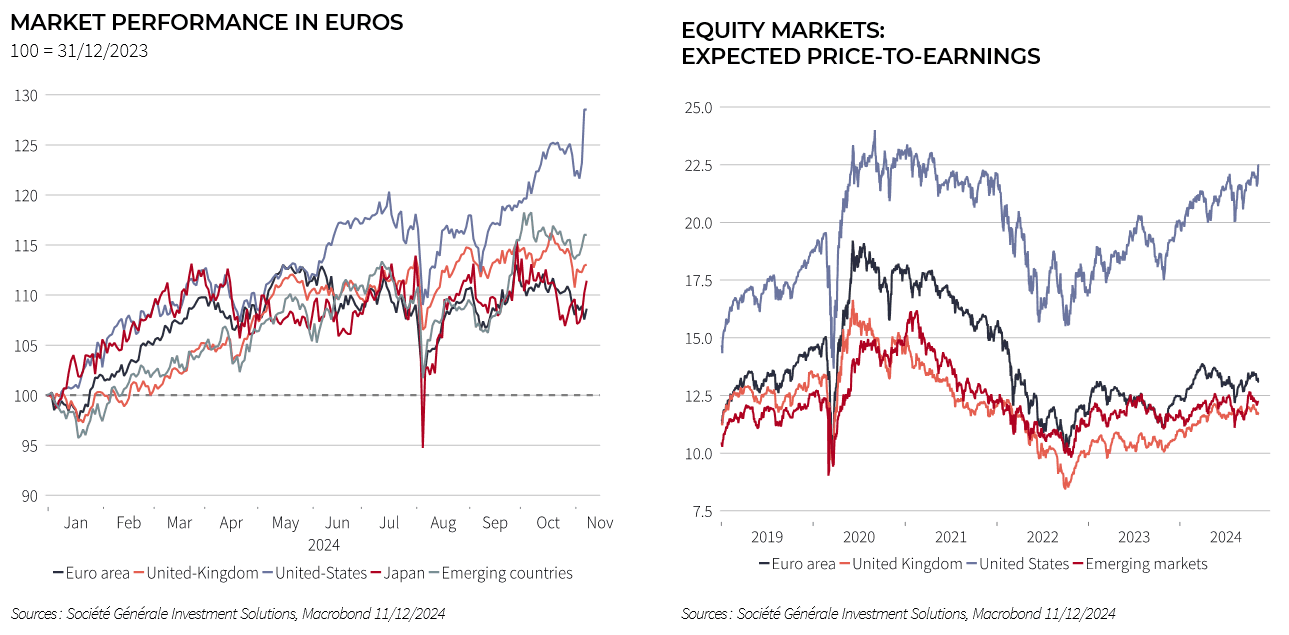

Euro Area. European equities had a more mixed performance (+1.7% since the US election), but growth stocks rose sharply. In the weeks ahead, euro area equities could continue to benefit, albeit to a lesser extent than in the US. They should also be supported by the improvement in monetary conditions (a fall in the euro and the prospect of rate cuts). Moreover, we expect household consumption to rebound in the months ahead, with falling inflation boosting households’ purchasing power. Finally, euro area equity market valuations remain attractive compared with the US. We therefore maintain a positive view on European equity markets but choosing sectors or companies that would not suffer from tariff hikes, such as the media, industry, and materials, and favouring companies that produce locally. However, we remain rather defensive and diversified, favouring large caps, in particular.

UK. Since Trump's election, UK equities have performed better than their euro area counterparts, but not as well as their US counterparts (2.5%). Given UK stocks’ high exposures to the US, the UK market rally should continue. The recent fall in the value of sterling and the - albeit gradual - rate cuts by the Bank of England will also be supportive factors. Moreover, the UK economy appears resilient, much more so than that of the euro area. Finally, as in the euro area, valuations on UK equities as a whole still appear attractive and as such we maintain a broadly positive outlook.

Japan. The Japanese equity market has slightly underperformed global markets since Trump's election (+2.8% vs. 3.6%) and since the start of the year (18% versus 22%). The past depreciation of the yen, improved corporate governance, and solid growth in corporate earnings should continue to support the Japanese market. Nevertheless, the volatility of the yen and the high proportion of technology stocks may continue to weigh on the market. We therefore keep a neutral outlook on Japan equities.