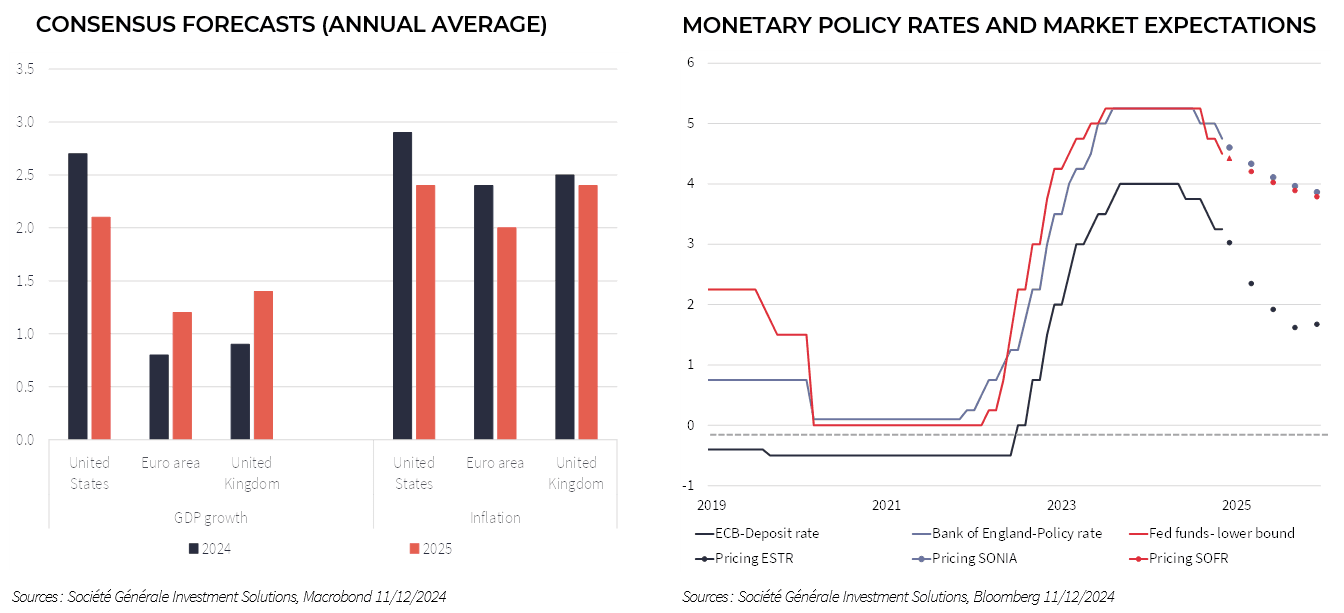

The economic trends observed in 2024 (outperformance of the United States, weakness in the euro area and China) are set to continue in 2025. This would allow central banks to continue their rate-cutting cycles, albeit more moderately for the Fed (3 cuts by the end of 2025) than for the ECB (5 cuts). Nevertheless, there are still many uncertainties surrounding economic policy, whether in the United States (tariffs, fiscal policy, or migration), Europe (French political situation, German elections) or China (timing and nature of the recovery plan).

United States: a robust economy, unless… The economists’ consensus forecast for 2025 is for continued vigorous growth in the United States (2.1% for the year). This performance would mark a slowdown compared with 2024 (around 2.7%), but only a moderate one, synonymous with a soft-landing. The US economy appears robust, benefiting from a number of favourable factors: healthy corporate and household finances, high productivity gains, and an expansionary fiscal policy.

However, the consensus forecasts are widely dispersed (from 1% to 3%). This is due to the uncertainties surrounding the measures to be implemented by the Trump administration (tax cuts, tariff hikes, etc.). For instance, a sharp rise in customs duties would ultimately have a major impact on inflation, penalising household consumption and hence growth. But the timing and scale of these measures remain hypothetical.

Slow decline in inflation. Given the strength of the economy, expansionary fiscal policy and the prospect of a trade war, the extent to which US inflation will continue to fall seems limited. Indeed, the consensus of economists does not forecast a return to the 2% target in 2025, but only a slight fall (2.4% after around 2.9% in 2024).

Euro area: growth continues to underperform. The consensus view among economists is for a slight improvement in the euro area economy, with growth of 1.2% for the year after 0.8% in 2024. However, this rebound would be mainly due to the expected (and partly technical) rebound of the German economy after a year of contraction in 2024. Moreover, this would mark a third year of weak growth and a continuation of its underperformance relative to the United States. This is the result of a number of factors, including weakness in the Chinese economy, political instability in France and Germany, and the prospect of higher US tariffs. However, falling inflation and ECB rate cuts should support household consumption and business investment.