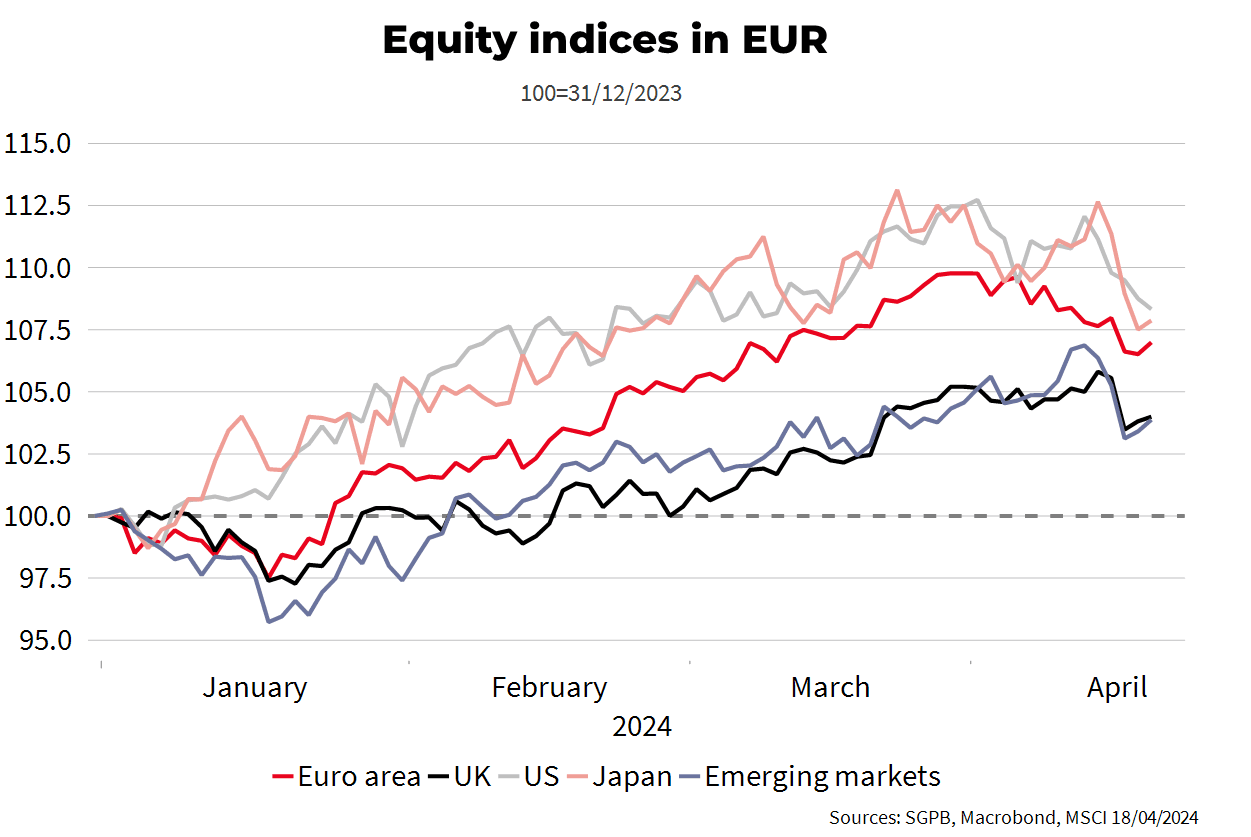

US. Having gained 10% in Q1, the US market lost around 3% last month, underperforming most of its major peers. Yet, its year-on-year performance remains impressive at over 20% and the correction has largely been driven by the downgrading of expectations for Fed rate cuts. Nevertheless, while its room for manoeuvre is shrinking, the Fed should still be able to trim rates in 2024. Also, US economic data continue to surprise on the upside, which should help sustain corporate profits. Stocks look expensive but momentum – measured as a 200-day moving average – and market sentiment remain bullish. We therefore stick with our Overweight on US equities. Our view on the artificial intelligence investment theme also gives us a heavier weighting to growth stocks.

Euro Area. European equities did well in Q1 and resisted well to the market correction, losing just under 0.5% on the month. In our view, they should continue to draw support from several factors. Valuations are attractive, market momentum is strong, and the economic bounce-back now seems locked in as the ECB is set to start its rate-cutting cycle in June – all of which is good news for corporate profits. We therefore remain Overweight European markets and, going forward, prefer growth stocks, which stand to gain most from the support factors mentioned above.