CIO Blog

February 2024

Tails of the Unexpected XI

Gene Salerno | Chief Investment Officer

Thomas Gehlen | Senior Market Strategist

Yvan Mamalet | Senior Economist & Strategist

SG Kleinwort Hambros CIO Blog February 2024

CIO Blog February 2024

Given the extraordinary circumstances and events of the past few years, this year might prove to be relatively quiet in comparison. Still, financial markets rarely fail to offer surprises, and 2024 is sure to offer its own unique twists and turns.

In the eleventh edition of our annual series “Tails of the Unexpected”, we consider a range of scenarios that are not part of the consensus thinking – or at least not yet. We also consider some of the implications for markets generally and SGKH portfolios more specifically, should these come to fruition.

This year, we are exploring the following (im-)possibilities.

After reaching more than 9% year-on-year in most advanced economies at the end of 2022, headline inflation has fallen significantly in 2023, hovering around 3% in the US and the Euro area and just below 4% in the UK1. Most of the relief came from lower energy prices and the normalisation of goods prices, while service prices inflation remained higher than pre-Covid levels. Markets appear to be pricing in a continuation of this downward trend, expecting inflation soon approaching the central banks' target. This, in turn, should allow central banks to begin their rate-cutting cycle as early as March.

1 Bloomberg, Bureau of Labor Statistics, UK Office for National Statistics, Eurostat

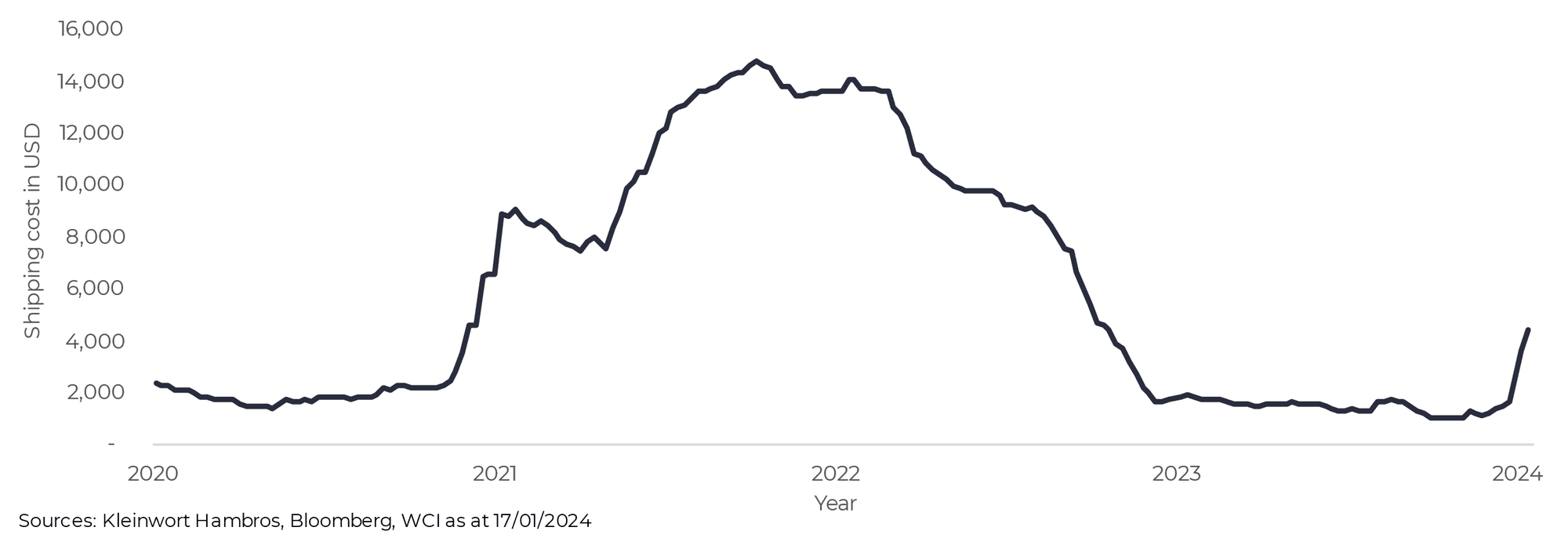

While peak inflation is most certainly behind us, upside risks to inflation persist. First, commodity prices are unpredictable, and a further surge in geopolitical risks could push oil prices back to (or above) the $100/bbl level. Second, if not eradicated, recent disruptions to trade routes (the Suez Canal for security reasons and the Panama Canal for drought) could lead to new supply chain tensions and, as a result, renewed upward pressures on goods prices. Finally, as the labour market remains tight in most advanced economies, wage growth may not moderate as steadily as markets and central banks expect. If these risks materialise, it could put central banks on their toes – limiting their room for manoeuvre, both in terms of the timing of the first cut and of the size of the easing cycle.

Equity and bond markets ended 2023 on a very strong note2, helped by expectations of a significant rate cut cycle. If inflationary pressures re-emerge and central banks fail to meet these expectations, the gains from late 2023 could be reversed. Sectors most sensitive to interest rates (e.g. utilities, real estate) and inflation (e.g. consumer goods) would be the hardest hit.

2 Bloomberg, MSCI

With our central scenario based on an economic soft landing, we see inflation continuing to decline gradually in 2024. This should allow central banks to pivot. However, they will remain cautious in the short term and any rate cuts will take place in small, slow steps – as opposed to a rapid easing phase. We therefore maintain a balanced portfolio allocation, neutral on equities but overweighted in bond markets, with a preference for corporate bonds.

Shipping Costs have Surged AgainCost per 40 ft container from Shanghai to Rotterdam, USD

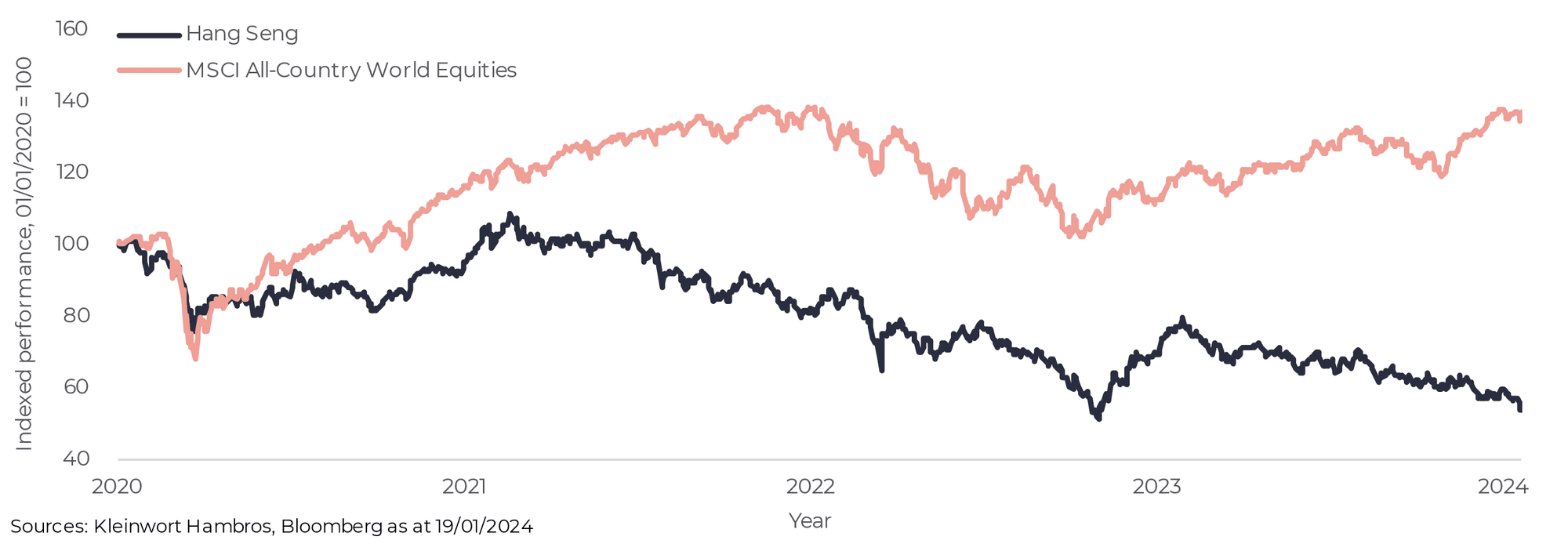

Global sentiment on Chinese markets has been dismal. Instead of a roaring recovery following the abandonment of the country’s restrictive zero-Covid policies in early 2023, investors faced the collapse of the biggest and second-biggest real estate developers, sluggish consumer spending, rising geopolitical tensions, and limited political action. Foreign investment dwindled, and the MSCI China index tracking the region’s A-share equities ended the year down -13.7%3. Decades of debt-fuelled economic expansion seem to be unravelling, and most expect the days of China as the driver of global growth to be numbered.

Indeed, China’s real estate sector, the economy’s trusty engine for growth, is now sputtering. Nonetheless, other parts of the economy are fast ramping up. Sustainable energy infrastructure is one of them: in the first quarter of 2023, the country’s capacity for solar power production reached 228 gigawatts, as much as the rest of the world combined. It is now producing ten times as many electric vehicles as Germany, and controls two-thirds of global lithium mining, a vital ingredient for battery production4. Tensions between the US and China have started to thaw, with Presidents Biden and Xi engaging in productive face-to-face meetings for the first time in a year back in November. This may be a boon not only for the Chinese economy, but global trade generally.

3 Bloomberg, MSCI4 Source: Bloomberg, Global Energy Monitor

After a protracted downturn since its peak in 2021, the Chinese equity market could be set for an epic rebound if sentiment recovers, rallying 50% from its relatively low base. Improving trade conditions and foreign investment would support the local economy and by extension its consumers. As consumer spending recovers, imports do as well, benefitting producers of cars, electronics, and luxury goods. Equity markets of major exporters such as South Korea, Japan, the US, and Germany gain 10%. On the flipside, bond yields rise 50 bps as rising commodity prices result in renewed inflationary pressure, forcing central banks to keep interest rates higher for longer.

Chinese Equities Significantly Underperformed Global PeersHang Seng and MSCI ACWI; Performance in local currency

A wide range of risky assets should benefit from a Chinese recovery. Equities would lead the charge in SGKH portfolios, led by our currently underweight but meaningful exposure to emerging market stocks, and followed by those regions set to benefit from rising exports, such as Japan, Europe, and the US. Climate - and growth-biased positions such as our Global Environmental Opportunities and Net Zero Ambition exposures should rally on recovering sentiment around the transition to a sustainable energy paradigm. This, in sum, is likely to vastly offset a marginal downturn on safe-haven assets such as government bonds as a result of rising yields.

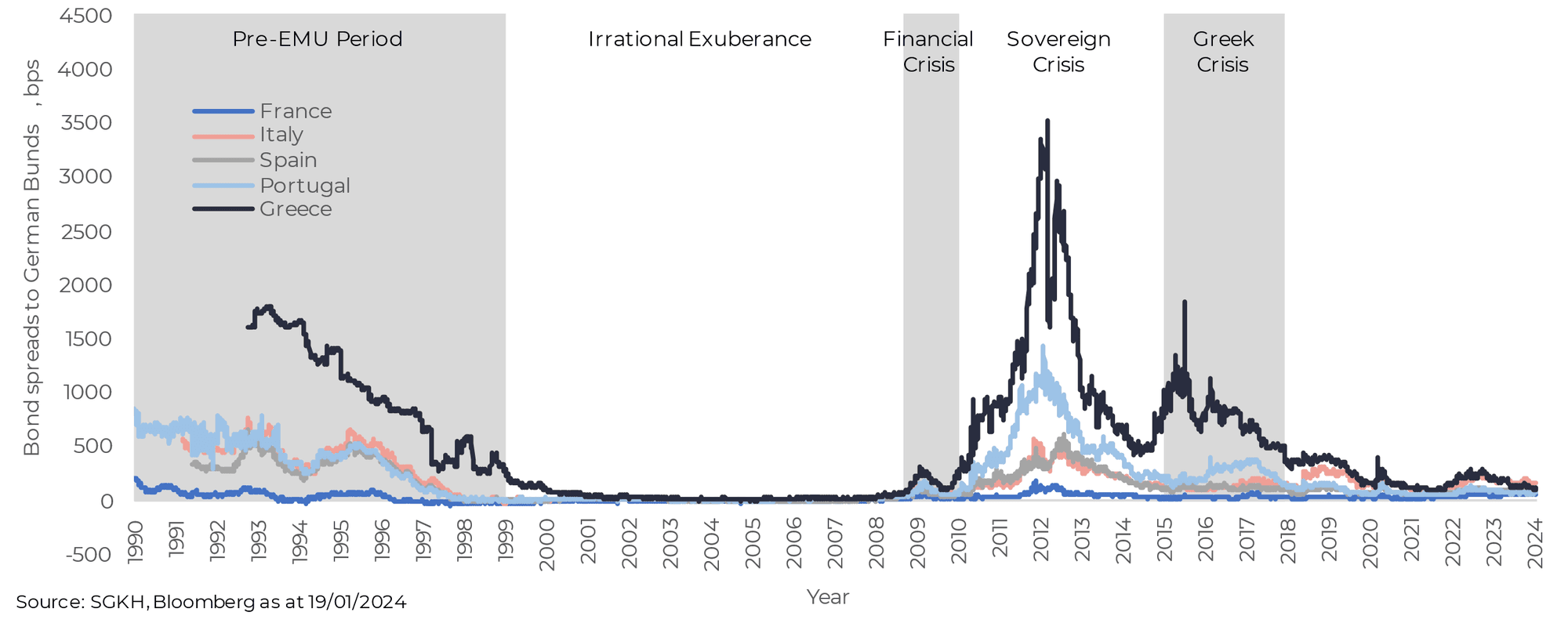

The euro area has come a long way from the fiscal uncertainty rocking the foundations of the monetary union more than a decade ago. Recently however, the zone has seen a sharp rise in ECB interest rates in 2023 despite slower economic growth, still high inflation for most of the year and several challenging political events at the local level (anti-pension reform demonstrations and suburban riots in France, hints at a new tax on banks in Italy, inconclusive elections in Spain, etc.)5. This led to high volatility of government bond spreads in the euro area during the year. However, spreads remain close to their five-year average pre-Covid levels (200 bps in Italy, 100 bps in Spain and 50 bps in France)6, highlighting that markets are not too concerned about the euro area member states’ fiscal path.

2024 may prove crunch time for euro area public finances. EU member states have agreed to reform fiscal rules, but the jury is still out on whether the changes could lead to more draconian or lenient fiscal policies over time. In any case, the old rules apply again this year – although not completely. More importantly, with more moderate nominal GDP growth and higher debt service, governments will face greater pressures to reduce their deficits. However, the political background in Europe is challenging to say the least. While Germany is about to embark on a new consolidation path, neither France, Italy nor Spain appear to be on the same track. Italy is considering a gradual transition to a flat tax; France faces ever-increasing demand for public goods despite already having one of the (if not the) highest public spending ratios in the EU, while Spain has rolled back some of the reforms that made its post-financial crisis glory. Finally, with the ECB announcing a faster reduction in its balance sheet7, member states will have to rely even less on it to finance their public deficits. Thus, in 2024 there may be renewed pressures on spreads, with high vulnerability to external shocks and/or political crisis.

5 European Central Bank, 6 Bloomberg, 7 European Central Bank

Renewed pressure on bond yields within the eurozone would mean bad news for European stocks (burdened by both confidence and subsequent austerity measures) and the euro (given renewed question marks over eurozone integration). German Bunds and CHF could instead benefit from this turbulence.

Eurozone Spreads Remain Far Below Crisis Levels (For Now)Euro area 10y sovereign bond spreads to German Bunds

Over the past twelve months we have reduced exposure to European equities due to a more challenging macro-economic backdrop. Indeed, tighter fiscal policy in the Eurozone is one of the reasons we see stronger GDP growth in the US than in Europe, and we prefer US stocks over European ones. However, we continue to monitor fiscal developments across Europe and are ready to re-allocate to the region should attractive opportunities emerge.

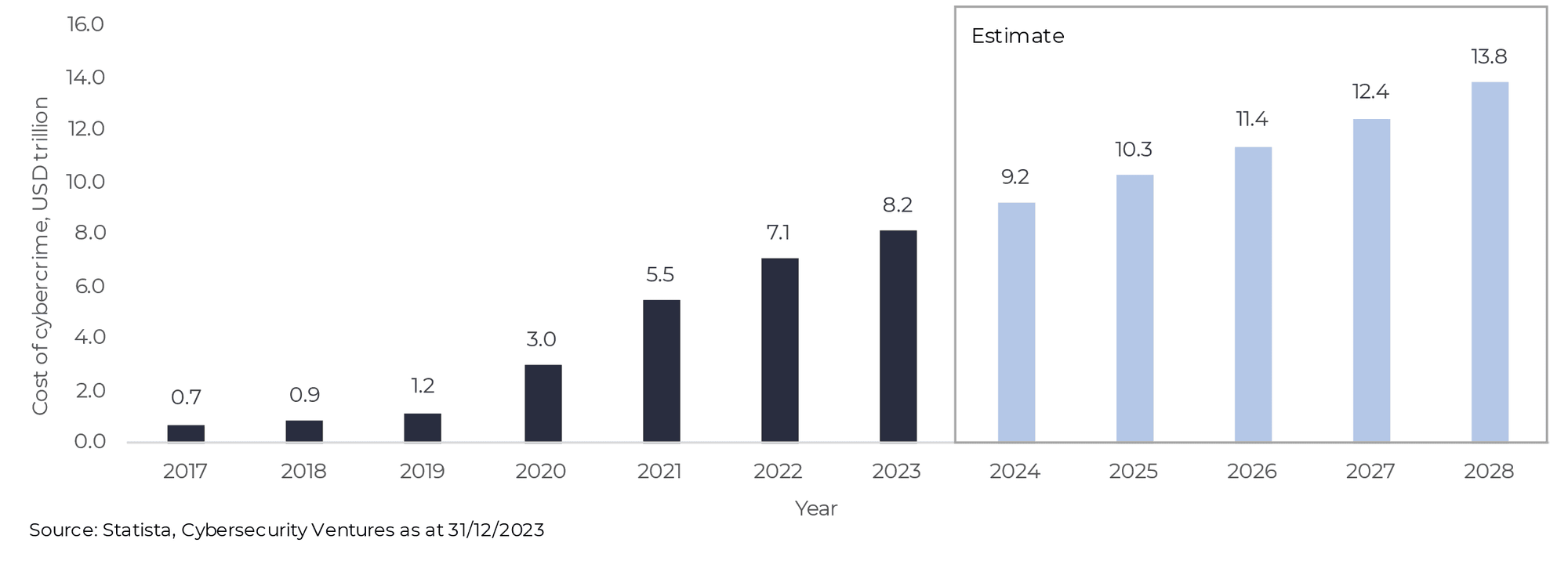

The estimated cost from cybercrime has risen more than tenfold over the past five years8. While cybersecurity has been an area of corporate focus for decades now, the acute move to remote working in the wake of the pandemic gave rise to a myriad of new vulnerabilities, waiting to be exploited. Four years on, security breaches are not unheard of, but many enterprises adjusted to the new environment by upgrading their defences to match more active foes. The damages from successful attacks will continue to rise in aggregate, but the pace of its growth is likely to slow.

While enterprises are beefing up their defences, digital criminals are exploring ever more ways to break them down. They may get tailwinds: a breakthrough in quantum computing, for example, could render the majority of existing data encryption procedures useless. Further, the continuing rise of generative artificial intelligence (AI) will enable more players to launch more attacks. Instead of a slowing pace of cyber security costs the global economy may experience a surge, as enterprises struggle with an explosion of digital damage, disruption, and theft.

8 Statista, Cybersecurity Ventures

The vast majority of enterprises in the western world are not sufficiently equipped for a new paradigm of cybercrime. Developed equities could drop 20% on a widespread campaign of malicious activity. Tech companies would suffer most under the additional threat to the intangible assets that make up the bulk of their valuations. The niche sector of information security players flourishes, with stock prices doubling. Elsewhere, safe haven assets such as government bonds and gold soar, with yields dropping below 2% in the US and UK and gold topping $2,200/troy ounce.

Estimates for the Growth in Cybercrime Damages Remain BenignEstimated cost of cybercrime worldwide; USD trillion

While SGKH portfolios are positioned for a cautiously optimistic outlook, they continue to hold significant safe haven exposures, including government bonds. Over the past two years we have gradually built up additional government bond exposure with increased interest rate sensitivity, which would benefit acutely from falling yields in the event of a systematic crisis. Funds running “alternative” strategies, such as those seeking to take advantage of mergers of large enterprises, could benefit from a rise in volatility and consolidation in the information security space. Within equities, we diversified away from the “magnificent seven” US tech companies (i.e., Apple, Amazon, Tesla, Meta, Nvidia, Alphabet, Microsoft) to limit portfolios’ concentration in vulnerable sectors, which should limit some of the downside in this scenario.

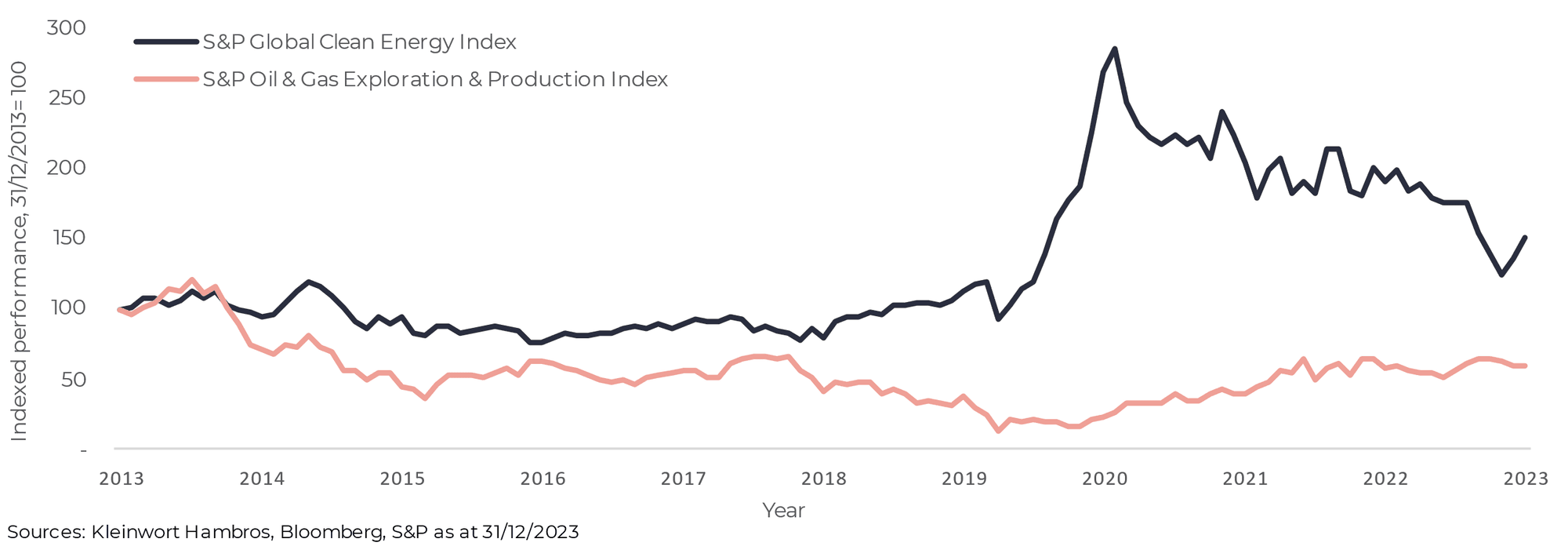

Investment in renewable energy and other environmental, social or governance (ESG) sectors have been suffering since the onset of the pandemic. Lofty valuations took a significant hit from surging interest rates. Worries around global warming have not disappeared but were superseded by more immediate challenges such as the Covid pandemic, armed conflict in Ukraine and Gaza, and the resulting impact on the cost of living across the western world. Governments’ priorities were firmly on securing energy supply for their citizens and industries rather than ensuring its sustainability: the US is now producing twice as much crude oil as it did a decade ago9; Germany has postponed its planned withdrawal from thermal coal production. Hopes – and valuations – of sustainable energy alternatives were dented.

With the likely end of the monetary tightening cycle amidst a normalisation of the highly inflationary environment, markets have begun to acclimatise to a new normal of elevated geopolitical uncertainty and interest rates. This has restored investors’ bandwidth for long-term investment strategy. A catalyst such as a major breakthrough in renewable energy technology – e.g., commercially viable nuclear fusion or a new generation of batteries - may spur an immediate and strong recovery of sentiment for the sector.

9 U.S. Energy Information Administration

Such a trigger event would drive general market enthusiasm, causing global equities to rally 10%. Renewable energy assets and the wider ESG sector would lead the charge, surging 25%, with industrials and auto sectors being dragged along. Infrastructure assets facilitating the Net Zero effort would benefit. The prospect of cheap, clean, and reliable energy supply is also inherently deflationary, easing the pressure on future monetary policy and, by extension, interest rates. On the flip side, constructing it will require immense amounts of capital, putting pressure on fiscal policy. The interplay between the two will make for continuing volatility in bond markets but also attractive opportunities in specific sectors.

Performance of Renewable and Traditional Energy StocksIndexed, 2013 to 2023. 31/12/2013=100

Responsible investing is a key component of the SG Kleinwort Hambros investment strategy. We continue to maintain targeted exposure to take advantage of the move to net zero, such as the Global Environmental Opportunities fund and S&P 500 Net Zero Ambitions tracker. Our allocation to real assets, specifically its position in renewable energy production and storage infrastructure, is set to gain significantly as well. Separately, SGKH’s sustainable investment process limits exposures to sectors like conventional oil and gas production and exploration, shielding portfolios from a potential downturn resulting from the emergence of sustainable alternatives.