Click the links to jump to a section, or flip the page to read all.

CURRENCIES

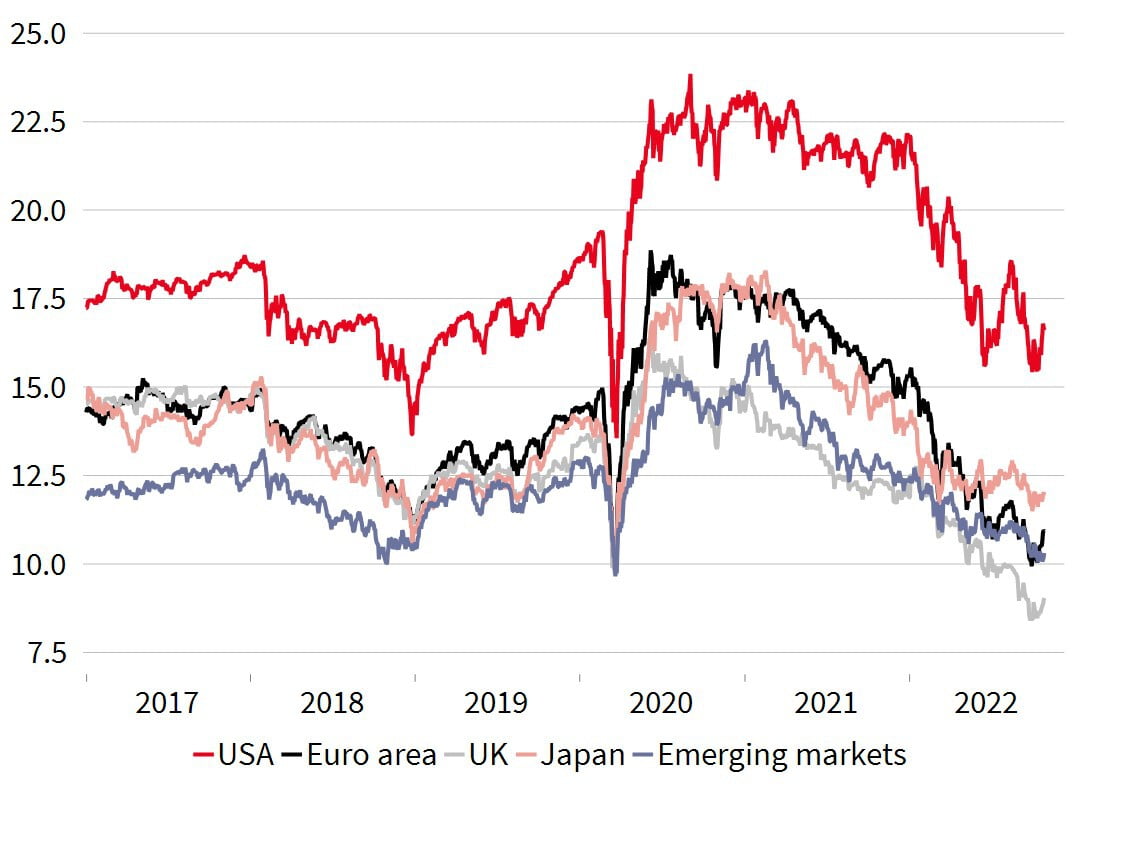

Equity markets rallied on expectations monetary tightening would peak in the next few months, however we see such expectations as premature and remain Underweight. We are adjusting our positioning within US equities to further reduce our exposure to Growth-biased sectors and hedged some more USD exposure.

United States. We remain at Underweight on US equities. The encouraging drop in inflation raised investors’ expectations for the Fed to pivot – i.e. slow or halt its rate rise cycle – given the implied slowdown in local and global growth. On the back of this sentiment, markets have posted their best single-day return since March 2020. However, Fed Chair Jerome Powell seems to be looking at inflation above his comfort zone for the foreseeable future and is likely to keep the monetary screws tight. We therefore retain our Underweight and continued to shift away from more growth-biased sectors that tend to be more sensitive to changes in interest rates.

United Kingdom. Despite the political crisis, British capital markets have continued to hold up relatively well since the start of 2022. Because of its sector specialisation, the UK stock market gets a boost from the general rise in commodity and energy prices, although the latter have eased back since the end of northern hemisphere summer. This relatively resilient performance should continue over coming months, despite the common risks to all equity markets and we remain Overweight.

Eurozone. Equities in the Eurozone have been rallying hard since the start of October, rising up to 12% from recent lows on hopes that rising gas stocks and falling energy prices will prevent power cuts this winter. The fading of British political risks has also helped. But inflation is still on the rise in Europe and could persist through 2023, prompting the ECB to keep monetary conditions tight. We remain Neutral.

Despite the political crisis, British capital markets have continued to hold up relatively well since the start of 2022.

Japan. We remain Underweight on Japanese equities. Japanese inflation is relatively low, with underlying price rises below their 2% target. While the world's leading central banks have been hiking rates, the Bank of Japan has stuck by its yield curve control policy, which targets a JGB yield of 0.25%. This policy continues to undermine the yen, which hit a 30-year low in October despite the Bank of Japan wading into currency markets on multiple occasions. The weak yen remains bad for Japanese equity markets and we are therefore taking a prudent line.

Emerging markets. The growth outlook remains challenging in emerging markets, particularly China. The US Federal Reserve’s relatively more hawkish approach has driven down emerging market currencies and the Chinese property sector is looking fragile. On the other hand, South American economies have been benefitting from elevated commodity prices and proactive monetary policy. We therefore remain Neutral on this market.

MSCI 12m forwards Price to Earnings ratio

Source: SGPB, Bloomberg, 27/10/2022.

Past performance does not prejudge future performance. Investments may be subject to market fluctuations, and the price and value of investments and the resulting revenues may fluctuate downward and upward. Your capital is not protected and original investments may not be recovered.

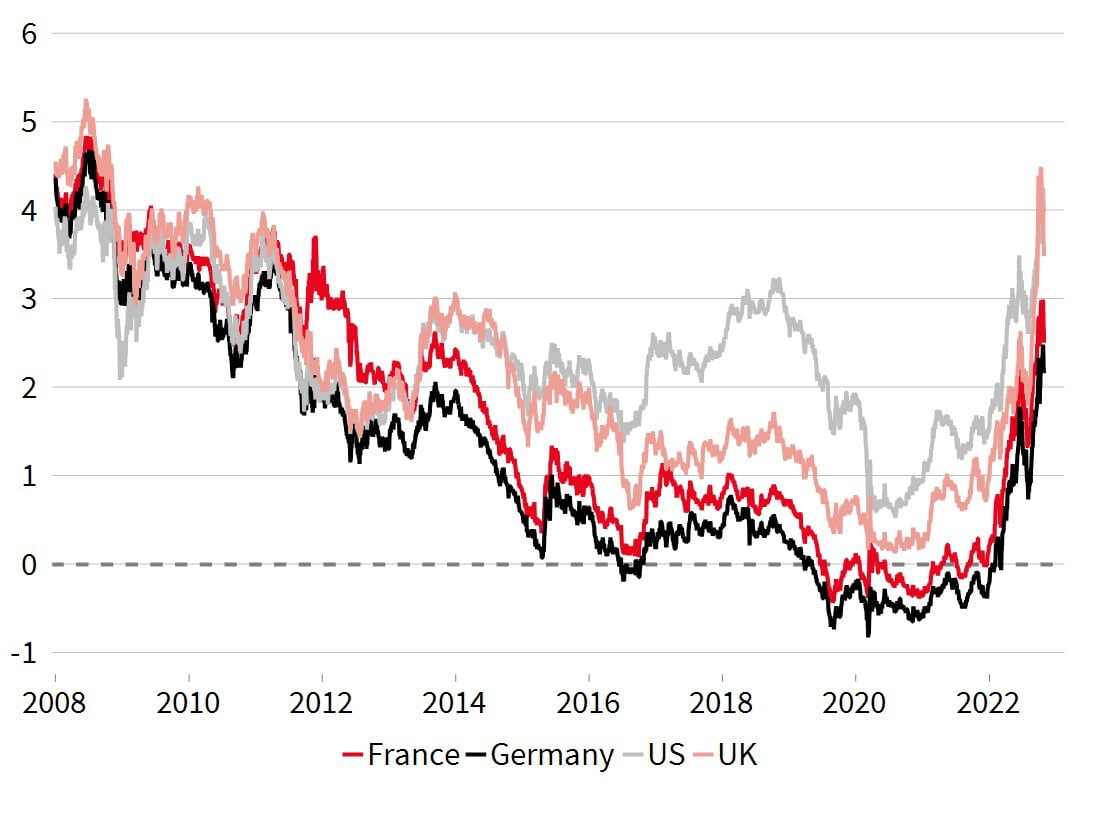

While we remain Underweight Fixed Income overall, we have gradually returned to a Neutral stance in Government Bonds amid a marked slump in global growth. We remain Cautious on Credit, especially High Yield, given deep uncertainties surrounding the economic environment.

United States. Sovereign bond yields dropped markedly from their peak of 4.2% (10-year) following an encouraging slowdown in core inflation figures, which at 6.3% came in significantly below expectations. Nonetheless, the Fed’s job is far from done and, although the expectations towards their terminal rate dropped below 5% (upper band) in Q1-23, rate cuts are not projected before 2024. At the same time, the yield curve remains highly inverted due to the risk of a more pronounced economic slowdown. Against this backdrop of already high rates and a sharp deterioration in the global outlook, we are Neutral on US government bonds (Treasuries).

United Kingdom. British sovereign debt has whiplashed throughout the autumn and the daily volatility index for gilts hit its highest since the series began. Initially, yields on the 10-year note shot up to 4.5% after the announcement of a fiscal stimulus package triggered a political crisis. Yields then fell back once Rishi Sunak became prime minister and committed to a more fiscally conservative line. Overall, although risks remain high given the country’s political instability and broader reliance on external finance, we are Neutral. Much of the adjustment now seems to have happened and the Bank of England seems willing to continue acting as lender of last resort if needed.

Eurozone. Sovereign yields rose last month as central banks tightened policy in the face of still rising inflation. Inflation remains high, 10% in September, or 4.8% once energy and food are stripped out. Even though energy prices have fallen substantially in recent weeks and this, coupled with some government measures, should help counter inflation over the next few months, underlying pressures and second-round effects remain strong. In these circumstances, the ECB accelerated its policy tightening, opting for a second 75 bp hike on all of its rates at its end-October meeting. Markets foresee a terminal deposit rate of 2.5%. The ECB will also disclose information about their balance sheet at its next meeting. As inflation does not yet seem to have peaked, we are Neutral on sovereign debt.

Developed markets. Stable nominal growth and elevated yields seem attractive for the time being, however, we remain cautious given the impending recession. We remain Underweight on Investment Grade credit and strongly underweight riskier segments such as High Yield.

Emerging markets. We remain Underweight emerging market debt. Monetary tightening in developed economies is generally bad news for emerging market assets and risks to growth remain high.

Government 10 year rates

Sources: SGPB, Macrobond, U.S. Department of Treasury 27/10/2022.

We remain Cautious on Credit, especially High Yield, given deep uncertainties surrounding the economic environment.

Past performance should not be seen as an indication of future performance. Investments may be subject to market fluctuations, and the price and value of investments and the income derived from them can go down as well as up. Your capital may be at risk, and you may not get back the amount you invest.

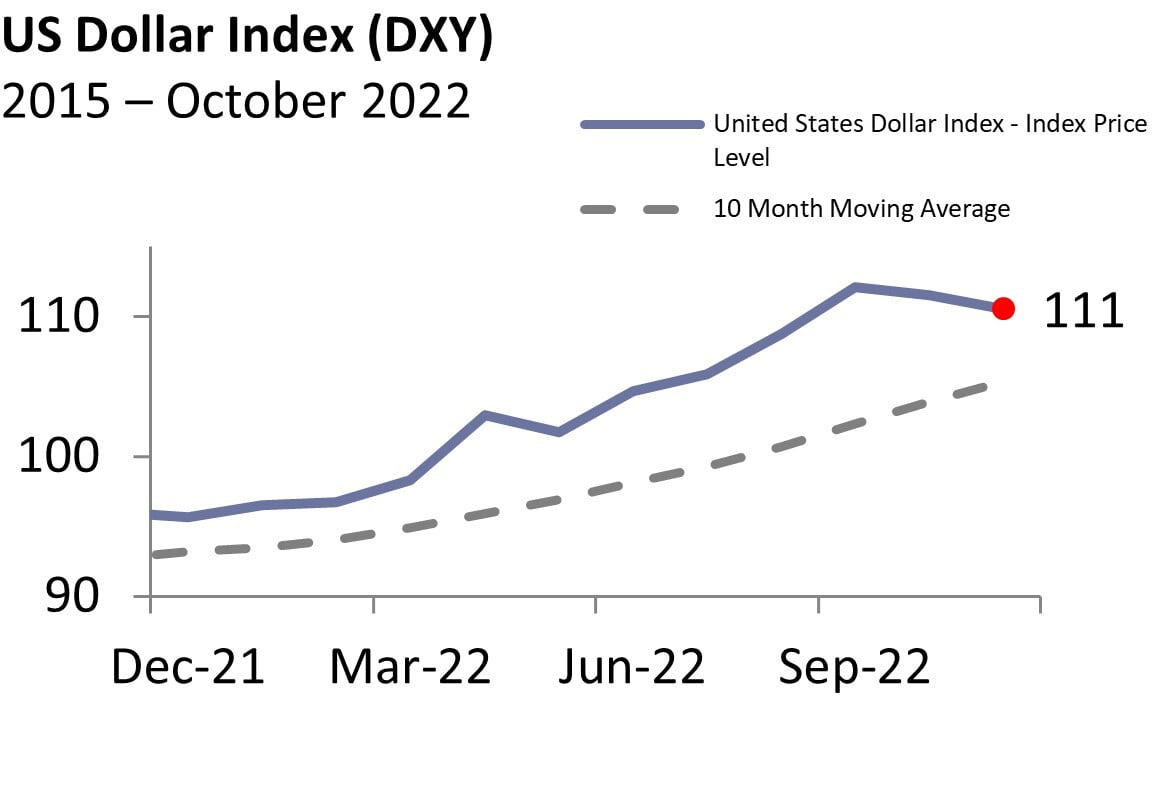

US inflation data for October came in lower than expected at 7.7% vs. 8.1%, this has given a relief rally to the market and is likely to mean a less aggressive Fed, causing the Dollar to weaken from its highs. Despite the weaker Dollar one has to remember that inflation does remain well above the 2% target so it might be too early to call victory on the inflation front which is likely to keep the Dollar higher vs. other currencies. We are looking to reduce our Dollar exposure and increase Sterling.

Dollar index (DXY). In recent weeks, the dollar has fallen back against major developed world currencies as inflation appears to be tempering. However, the feeble outlook for global growth, harder-than-expected policy tightening by the Fed compared to other central banks and ongoing political risks will continue to buoy the greenback.

EUR/USD. The euro rose in recent weeks, back to dollar parity. Its new-found strength reflects a major drop in European electricity prices driven by higher-than-expected gas reserves and a warm autumn. The speeding up of the ECB's monetary policy tightening was good for the euro.

GBP/USD. The pound surged up and down in the wake of gilt movements, touching all-time lows against the dollar at the end of September 1.03 but has since rallied to 1.17 GBP/USD. The temporary fix to the political crisis and return of a fiscally conservative policy mix allowed the GBP to revive. Falling energy prices also helped the pound, like the euro. Our strategies have profited over the last few years being overweight the dollar. Now, to limit the likely headwind facing an extremely weak pound and the mean reverting nature of currencies, we continue to look to reduce our dollar exposure and increase our sterling exposure.

USD/JPY. Downside pressures on the yen, now at its lowest since 1998, remain significant. The Bank of Japan has left monetary policy unchanged as underlying inflation remains weak. To address downside pressures on the yen, the monetary authorities are instead intervening directly in currency markets by selling dollar assets.

US Dollar has fallen from its peak

Source: Bloomberg, Kleinwort Hambros, Data as at 10/11/2022.

Emerging market currencies. Emerging currencies rose over the month having their biggest jump since 2016. China appears to be easing some of its draconian lock-down rules and the dollar strength could potentially be falling from its peak due to a lower-than-expected inflation number. A slower pace of US hikes may offer some respite for emerging-market assets.

Recent months have shown how important it is to have alternative assets in a portfolio. Our hedge funds allocation has performed well despite the market sell-off and gold provided another layer of much needed diversification with its best weekly performance in two years. We continue to hold an allocation to real assets and our Tail Risk Protection Note.

Oil. OPEC announced it was cutting supply by 2 million barrels/day to reflect the fall in demand as the global economy slows. This allowed the oil price to stabilise at around USD 90/bbl. If China were to ease more of its lockdown measures this would put upward pressure on Oil. At the same time, a global recession fears would inevitably mean less demand for Oil.

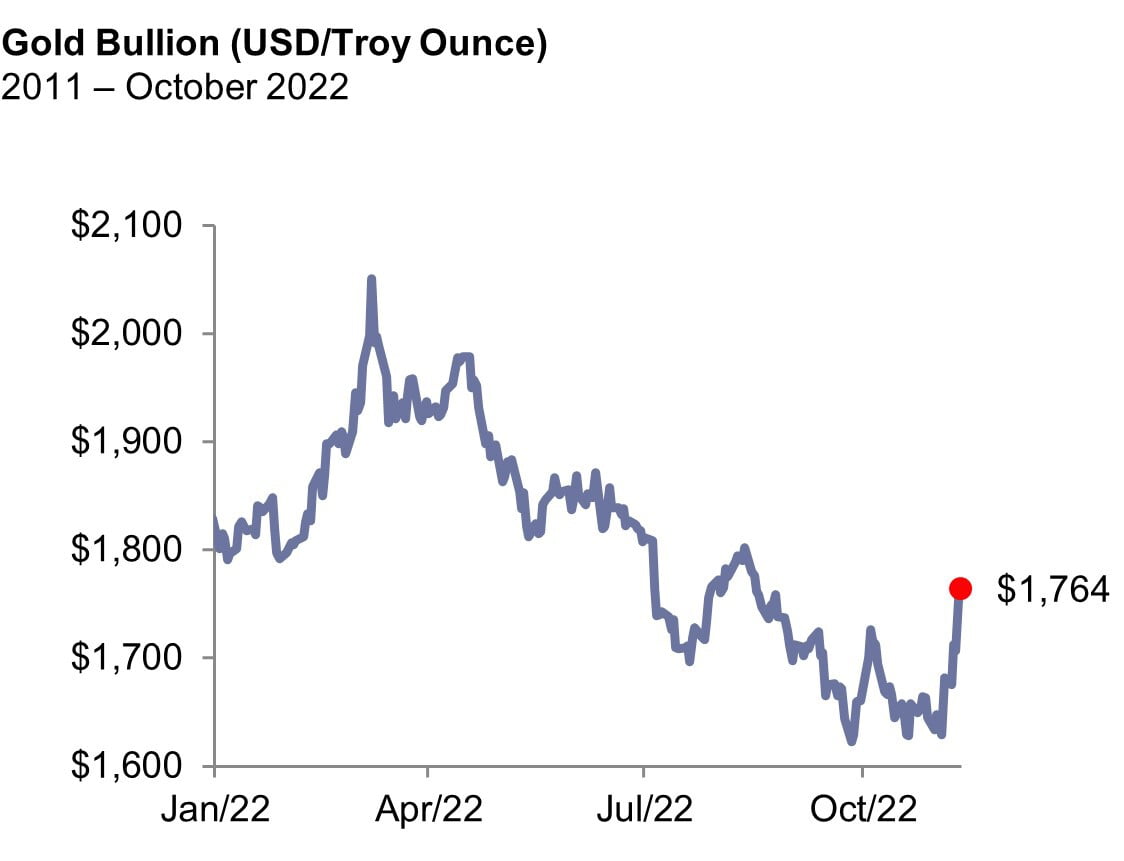

Gold. The precious metal had its best week in more than two years after inflation data cooled slightly meaning a less aggressive Fed. Gold now trades at $1765/oz. A falling dollar is helping gold rise. We remain overweight gold given the general economic slowdown as it remains a good source of diversification in volatile times.

Gold has best week in more than two years

Hedge Funds. In unstable market conditions hedge funds can help a portfolio, but selectivity is key. We prefer strategies which hold their own in bear markets, such as Merger Arbitrage, trend followers and Equity long/short. These strategies provide relatively safe, uncorrelated sources of returns from equities. Our hedge funds allocation has performed well over the year and been a great diversifier in our strategies.

Real Assets. We continue to allocate to a diversified portfolio of infrastructure (such as energy storage and efficiency, smart grids, waste-to-energy, air treatment and digital infrastructure) and specialist property assets (including affordable housing, care homes and e-commerce and logistics warehouses). These real assets offer additional diversification from other risk assets such as equities, as well as an attractive income stream and reasonable sensitivity to inflation.

Tail Risk Protection Note. Tail risks are typically understood as unlikely but severe crisis events which shock markets and dramatically impact the value of risk assets negatively. The dot-com bust at the turn of the century and the Great Financial Crisis in 2008 and 2009 are examples of such events. Despite it not performing well over the year, we believe the Tail Risk Protection Note offers our portfolios yet another critical source of safety and complements the existing diversifiers.