Click the links to jump to a section, or flip the page to read all.

CURRENCIES

In a still uncertain environment, we remain generally cautious on equity markets. UK and European markets seem to have largely priced in the likely recession, however uncertainties remain significant and we are sticking to a prudent Underweight position for the time being.

United States. We remain Underweight United States equities. US stock market indices continued their October rallies in November, helped by good inflation figures and broadly accommodative statements from Federal Reserve chairs. However, we think substantial risks continue to overshadow US equity markets. The consensus expects the United States economy to grow 0.4% in 2023, but risks are mainly on the downside and corporate earnings are showing the first signs of slowing. We have therefore opted to remain cautious.

United Kingdom. The UK stock market has outperformed all other developed economies in 2022, thanks to its focus on energy and commodities sectors, vindicating our decision to retain a relatively high weighting. While recent political disruption and the easing of pressure on commodity markets have not been good for UK equity indices, the market has still managed to put on nearly 9% so far in Q4. Also, investors are now nearly unanimous in expecting the UK to slip into recession in 2023, which puts a floor under risks of revenues disappointing. We therefore maintain our Overweight exposure to this market.

Eurozone. Eurozone indices did well during the recent rally. Indeed, the area's market has outperformed the United States’ in the year to date. Consensus projections now factor in a moderate recession in 2023 and latest data for underlying inflation suggest pressures continue to run high. Also, the Ukraine war remains profoundly uncertain. Having said all that, European economies today are proving remarkably resilient, as evidenced by the recent upgrades to German and Italian Q3 growth. We think this resilience could well persist and potentially force markets to upgrade their (pessimistic) earnings estimates for 2023. We are Neutral.

While recent political disruption and the easing of pressure on commodity markets have not been good for UK equity indices, the market has still managed to put on nearly 9% so far in Q4.

Japan. We remain Underweight on Japanese equities. Revenues from overseas investments remain strong and show no sign of flagging, underlining Japanese companies’ ability to ride out the contraction in activity. The yen is likely to remain weak against the major currencies, however, which leads us to remain cautious about putting money into the Japanese market.

Emerging markets. Social unrest in China has added another aspect to uncertainty in the economy, though the Communist Party’s signalling of a shift in its Covid policy sent markets soaring. Emerging market currencies have been weakened by the Fed’s monetary policy tightening, creating attractive opportunities in the space. We are Neutral.

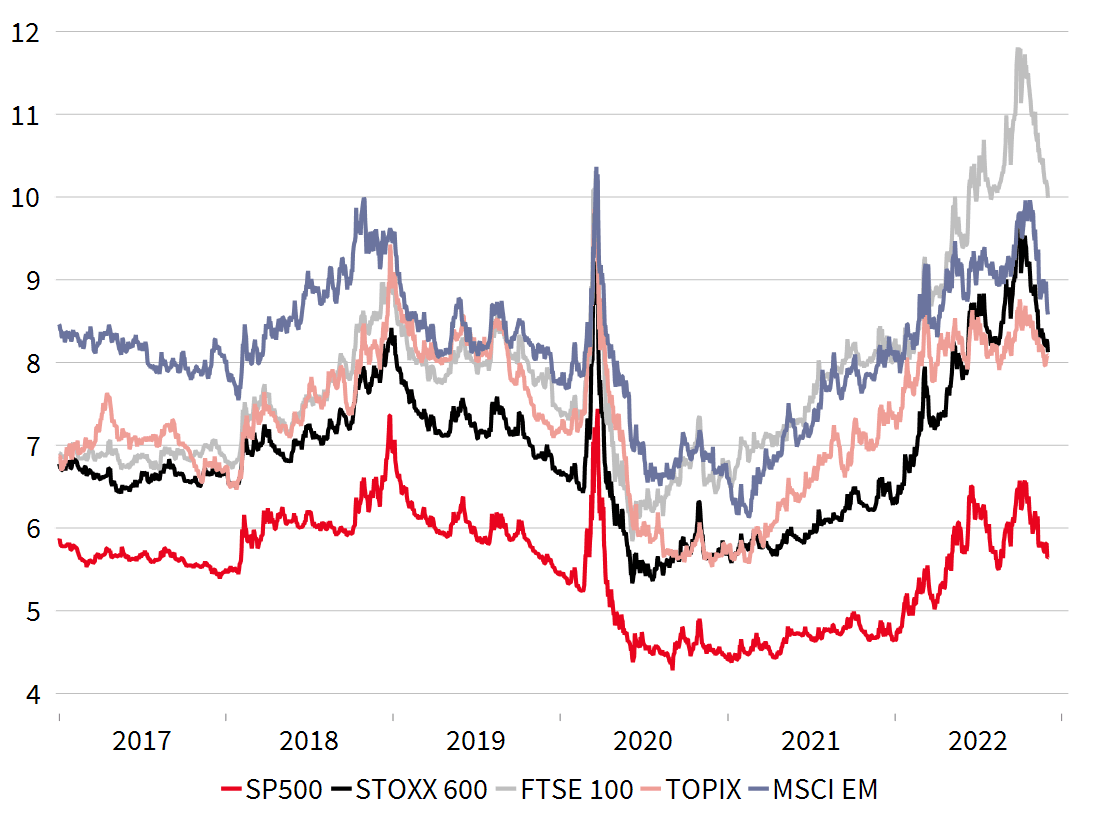

Equity earnings yield (Earnings per Share/Share Price)

Source: SGPB, Macrobond, MSCI 30/11/2022

Past performance does not prejudge future performance. Investments may be subject to market fluctuations, and the price and value of investments and the resulting revenues may fluctuate downward and upward. Your capital is not protected and original investments may not be recovered.

We remain Neutral on developed government bonds in an environment of deteriorating global growth and positive real rates. Further, we have taken advantage of the past few months’ yield easing and shortened our duration positioning to underweight.

United States. After a period of sustained increases, Treasury yields edged back last month. The 10-year yield fell to 3.5% by early December from 4.2% in mid-October. The main reason was confirmation that headline and core inflation have indeed peaked over the autumn and are now likely on a gradual downward track. This pressure-drop in inflation should give the Fed leeway to relax the pace of its rate hikes, tightening by “just” 50 bp in December to a terminal rate of 5%, expected some time in Q1 2023. Fears of a sharp slump in the US and global economies have also helped drive yields down. We, however, think underlying inflation will take time to diminish, leading the Fed to keep a tight rein on financing conditions throughout much of 2023. Against this backdrop and given the Fed's determination to keep real rates positive across the whole curve we are maintaining our Neutral position to Treasuries.

United Kingdom. Gilt yields have continued to fall back since the fiasco of the September budget, with the 10-year yield down from 4.5% to 3.1%. Rishi Sunak's new government has announced a new and net restrictive budget, freezing spending and leaving taxes largely unchanged for the time being, which has been well received by markets. The Bank of England also announced it was slowing the pace of its rate rises in light of the feeble growth outlook for the British economy and the systemic risk that higher rates pose to households mired in floating-rate debt. Also, as in the euro area, real rates remain close to zero. We remain Neutral.

Eurozone. Euro area sovereign debt yields also declined in November. The Bund 10Y dropped from 2.5% to 1.9% and the OAT 10Y from 3% to 2.4%. The story was similar in peripheral sovereign markets, with Italian 10-year BTP yields down to 3.8% narrowing the spread to the bund to 190 bp compared to 250 bp in September. As in the United States, this is being driven by a better outlook for inflation as energy prices come down. In Europe, natural gas prices have dropped nearly 60% from their summer peak with reserves now at all-time highs and the weather remaining unseasonably mild. The resulting dip in inflation should allow the ECB to slow the pace of its rate hikes, with a 50 bp rise expected in December and a terminal deposit rate of 2.75% some time in 2023. While nominal rates have risen substantially, real rates remain near zero and we are maintaining our Neutral stance on European sovereign bonds.

Developed markets. Stable nominal growth and elevated yields seem attractive for the time being, however, we remain cautious given the impending recession. We remain Underweight on Investment Grade credit and strongly underweight riskier segments such as High Yield.

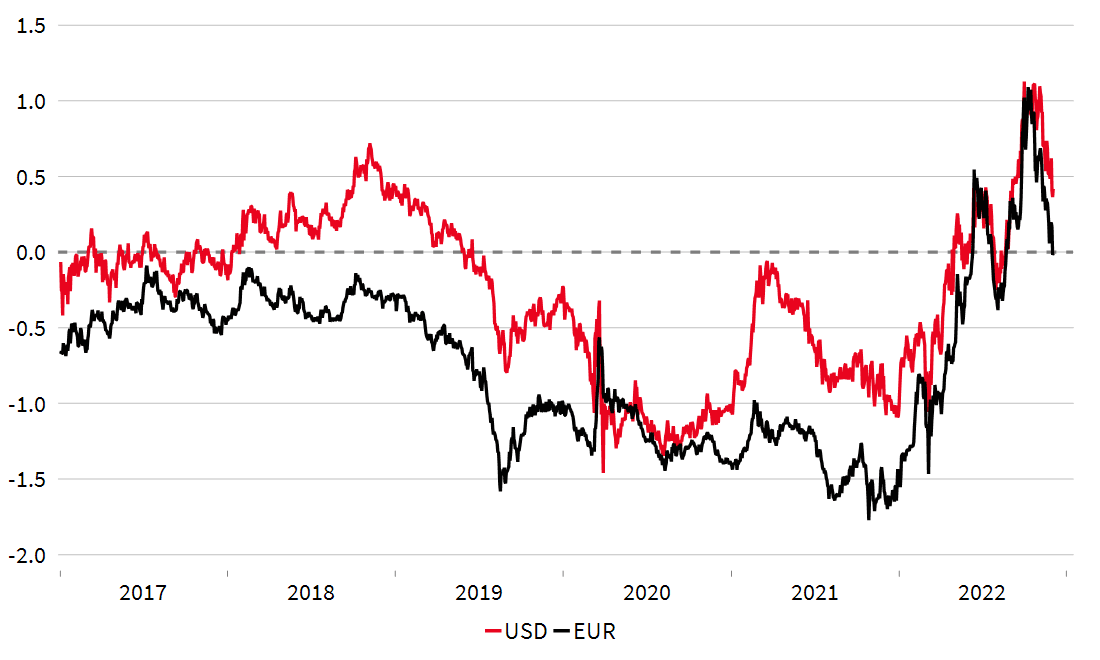

Real rates OIS swap-inflation swap

Sources: SGPB, Bloomberg, 28/10/2021

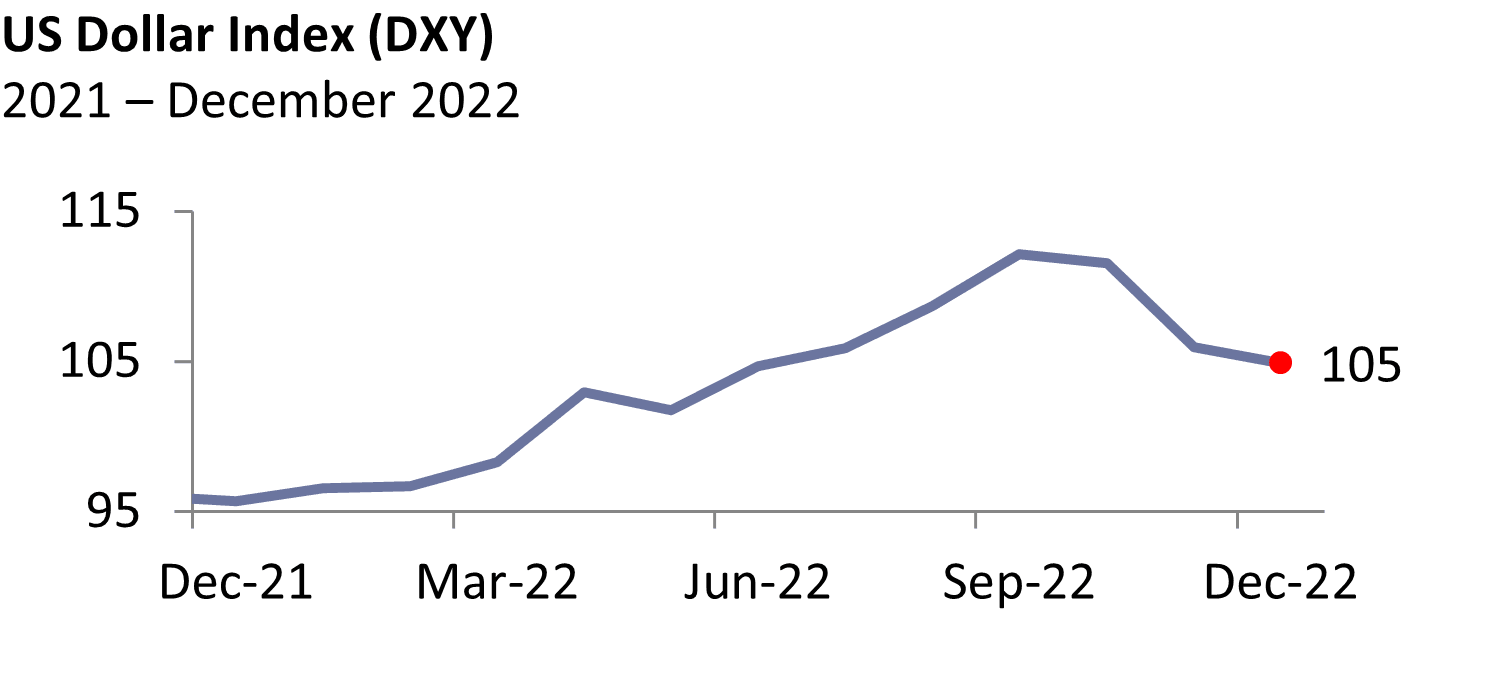

The market expects the Federal Reserve to start slowing the pace of its interest-rate hiking due to falling headline inflation. This has weakened the value of the Dollar from its heights and over the month of November, posting its worst month in over 12 years (falling -5%).

GBP/USD. Sterling gained 5% over the past month against the dollar, benefiting from lower energy prices and the prospect of a less aggressive Fed. In addition, the easing of financial tensions following the new budget announcement also helped the pound gain ground and it has appreciated +14.3% from September lows.

EUR/USD. The European currency continued to appreciate against the dollar (+5.7% month-on-month), stabilizing at 1.03 against a backdrop of falling energy prices in Europe and an expected slowdown in the pace of Fed rate hikes. We believe that the interest rate differential between the US and the Eurozone will continue to narrow, supporting the European currency further. Furthermore, the bulk of the deterioration in European external accounts has likely passed, with gas and energy prices expected to remain below their summer peak due the high level of inventories. Without renewed geopolitical tensions or sharp declines in temperatures, this should support the euro.

USD/JPY. The downward pressure on the yen has diminished significantly over the past few weeks, with the Japanese currency even appreciating by 6% against the dollar. The Bank of Japan is expected to only gradually increase sovereign rate targets as part of its curve control.

Dollar index (DXY). The dollar continued to decline against the major developed and emerging currencies over the past month. The moderation of inflation in the US, implying the expectation of a slowdown in Fed tightening, supported the currencies of the developed economies.

The Dollar has a further month of weakness

Source: Bloomberg, Kleinwort Hambros, Data as at 08/12/2022

Emerging market currencies. Emerging currencies continued to strengthen throughout November. New policies indicated by the Chinese Communist Party seem to suggest a less stringent approach to Covid restrictions, suggesting a re-opening of one of the world’s largest economies. In the short term it is likely that these measures will lead to an increase in infections but as herd immunity takes over, like it did in the West, this should start to ease. Geopolitical tensions over trade and Chinese Tech companies remain between the US and China, which could weigh on EM currencies.

Oil prices weakened amidst elevated risks of a global recession, particularly in China where growth is at risk of slowing significantly despite a somewhat more promising Covid policy. Gold should continue to play its role as a safe-haven. We continue to hold our allocation to Real Assets and our Tail Risk Protection Note.

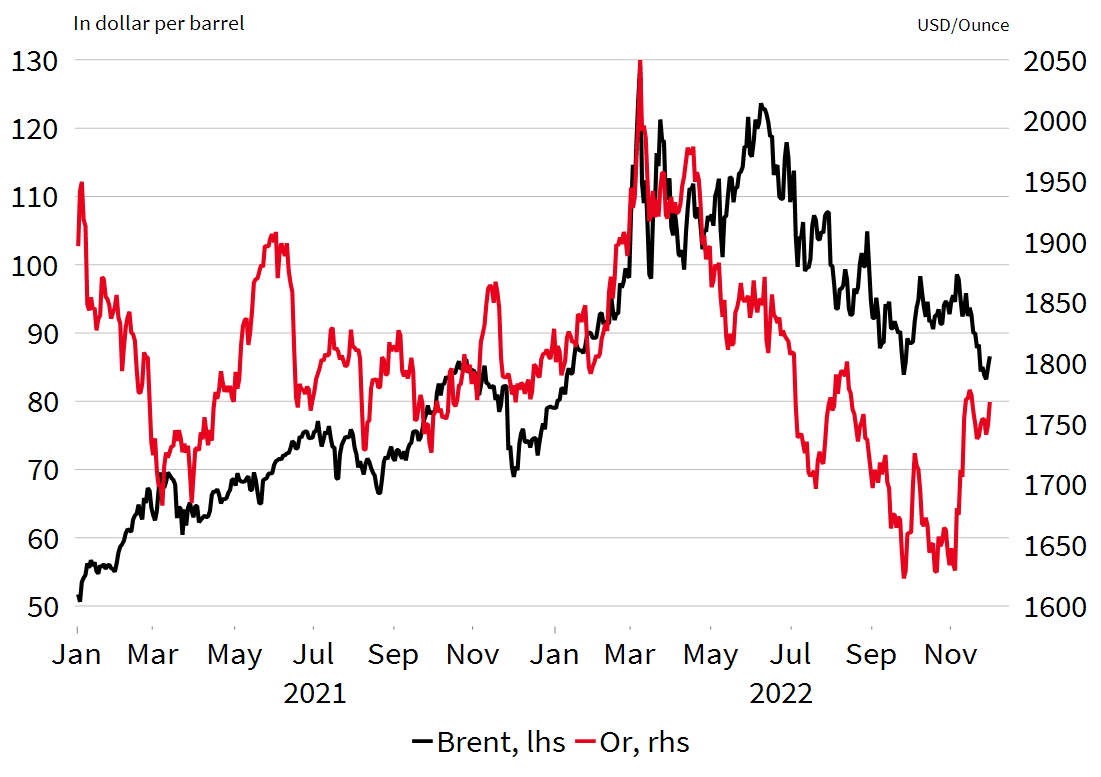

Oil. Fears of a recession in 2023 have pushed the price of oil down 5.4% since the beginning of the fourth quarter. The commodity also remains highly dependent on decisions by the Organization of the Petroleum Exporting Countries (OPEC) and revisions to growth forecasts for 2023. The evolution of Chinese activity will be particularly important, and a stronger-than-expected slowdown could weigh on the oil price.

Gold. Central Banks as a group bought more gold in Q3 of 2022 than ever before – a record 399 tonnes, according to the World Gold Council. While there is speculation surrounding the real reason, this has generally benefited Gold. A stronger US dollar and the Federal Reserve’s aggressive monetary tightening, particularly since June, have until recently been a key headwind for the gold price whilst inflation has concurrently put upward pressure on costs. Looking forward though, the outlook for gold is stronger with the Fed expected to ease interest rate increases within 12 months as inflation reduces and the global economy is expected to slow significantly.

Price of Brent Barrel and Ounce of Gold

Sources: SGPB, Macrobond, ICE, EIA 30/11/2022

Hedge Funds. In unstable market conditions hedge funds can help a portfolio, but selectivity is key. We prefer strategies which hold their own in bear markets, such as Merger Arbitrage, trend followers and Equity long/short. These strategies provide relatively safe, uncorrelated sources of returns from equities. Our hedge funds allocation has performed well over the year and been a great diversifier in our strategies.

Real Assets. We hold an allocation to a diversified portfolio of infrastructure (such as energy storage and efficiency, smart grids, waste-to-energy, air treatment and digital infrastructure) and specialist property assets (including affordable housing, care homes and e-commerce and logistics warehouses). These real assets offer additional diversification from other risk assets such as equities, as well as an attractive income stream and reasonable sensitivity to inflation.

Tail Risk Protection Note. Tail risks are typically understood as unlikely but severe crisis events which shock markets and dramatically impact the value of risk assets negatively. The dot-com bust at the turn of the century and the Great Financial Crisis in 2008 and 2009 are examples of such events. Despite conditions not being favourable for it over the past twelve months, we believe the Tail Risk Protection Note offers our portfolios yet another critical source of safety and complements the existing diversifiers.