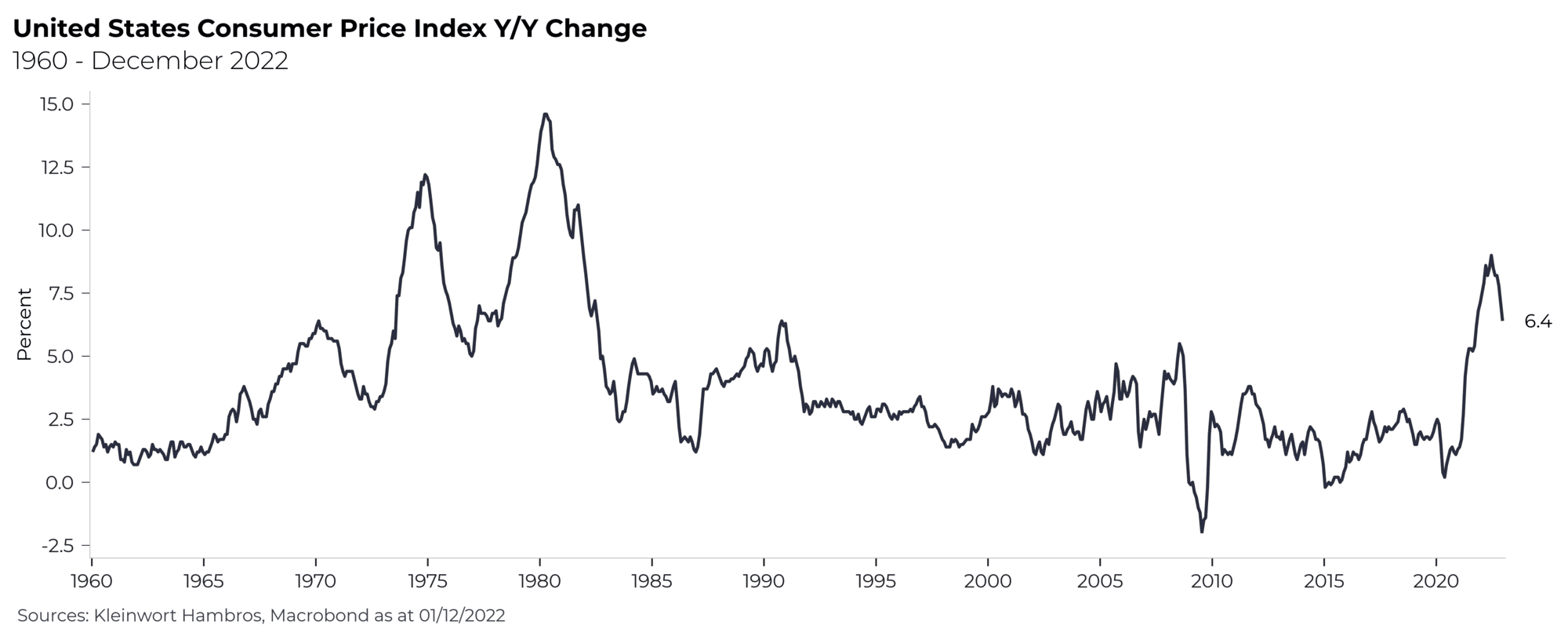

After 20 consecutive months of US inflation exceeding the Federal Reserve’s (Fed’s) 2% target, economists’ initial assessment of temporary price pressures is expected to finally come to pass in 2023. Pandemic-era supply chain issues have gradually dissipated, the initial energy shock in response to Russia’s invasion has worn off, and central banks’ coordinated efforts to tighten monetary policy and slow down their respective red-hot economies are beginning to bear fruit. The peak of price pressures seems to have passed, and economists expect inflation prints to gradually ease closer to the Fed’s target throughout 2023, paving the way for a widely expected monetary policy pivot.

While gold would face a hostile environment in this scenario, other safe havens such as hedge funds and our Tail Risk Protection Note would benefit from rising volatility and offset potential losses in other assets in the short term.

Despite the Fed’s best efforts to slow down the economy, consumer spending, supported by strong balance sheets, remains resilient and the labour market surprisingly tight, causing a wage-price spiral. House prices and the cost of shelter do not moderate as expected. The opening of the Chinese economy may cause havoc to supply chains in the short term and boost demand – especially for commodities – in the medium term; widgets such as semiconductors will again fall in short supply and headline inflation worries may well have another upswing. Far from a pivot, the Fed responds by turning more hawkish and further rate hikes take markets by surprise.

Yields on treasury bonds spike above 5% as the hope for a short-term Fed pivot evaporates. Bond prices, which move in the opposite direction of yields, drop, and the asset class resumes its worst momentum in more than a century. Equities drop another 15% as valuations reflect the prospect of sharper monetary tightening and heightened recession risks, and global sentiment is hit as investors get spooked by a rapidly changing economic environment and outsized market reactions. The dollar rallies on more attractive yields and gold softens to below $1,700 in response to forced collateral selling and rising opportunity costs.

We prefer a prudent stance given the still exceptional uncertainties surrounding the world economy. As a result, we remain underweight equities as an asset class, specifically with respect to US equities, whose valuations and sentiment has not yet bottomed to a similar degree as in other developed markets. Over the past few months, we have further reduced duration to reduce portfolios’ sensitivity to changes in yields, particularly those unfavourable moves outlined above. While gold would face a hostile environment in this scenario, other safe havens such as hedge funds and our Tail Risk Protection Note would benefit from rising volatility and offset potential losses in other assets in the short term.

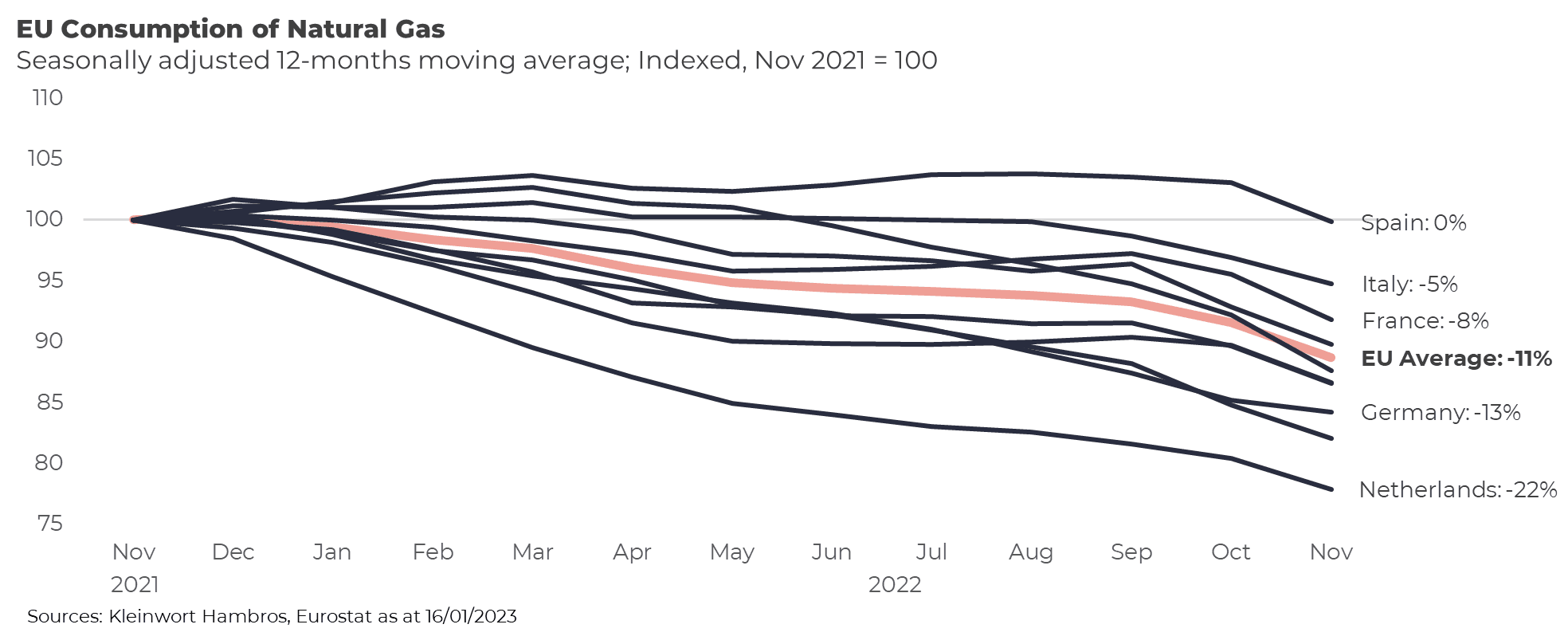

The forward curve shows that investors expect energy markets to stabilise in Europe given a mild winter and full gas storage coming into 2023. Indeed, industrial nations such as Germany weathered 2022 surprisingly well, relying on a combination of government subsidies, leaps in energy efficiency – German industries reduced gas demand by a quarter without significantly affecting output! – and luck granting the continent a largely mild winter. Gas storage remains filled above average, and tankers are coalescing outside newly constructed floating LNG terminals to dispense their load once storage levels begin to slump, promising a lid on prices in the short term.

The forward curve shows that investors expect energy markets to stabilise in Europe given a mild winter and full gas storage coming into 2023.

The extent to which European economies are reliant on Russian oil and gas might not fully be grasped until it is too late. Much of the gas filling the continent’s storage facilities in 2022 was supplied through Russian pipelines before firm embargoes were in place, and largely mild weather prevented a run on the supplies, reducing the risks of rationing and black outs. Circumstances may well not be as favourable in 2023: Russian supply has all but halted, and next winter’s weather remains unpredictable. Further, the Chinese economy’s re-opening is likely to stimulate global oil demand, resulting in additional price pressures around the world. European unity already appears stretched and a fiscal response of the same magnitude as that of yesteryear seems politically unpalatable, and both industry and households are likely to suffer should next winter prove colder than this one.

As opposed to their overseas colleagues, the European Central Bank (ECB) is largely powerless in curbing further inflationary pressures given the exogenous nature of their cause. Continental equity markets would be hardest hit, with the Eurostoxx posting another 20% downturn as the worst-case scenario that had largely been priced out during the latest relief rally re-enters the picture. Yields on euro-denominated debt drop and gold rallies as investors seek shelter from a spike in volatility and an increased likelihood of a deep European recession.

We are currently maintaining a Neutral position on European equities as sentiment has proven exceptionally bearish since the early days of the Russian invasion, resulting in attractive valuations across the continent. Uncertainties still run high specifically with respect to the ongoing conflict, leading us to maintain significant exposures to government debt as well as gold, which will provide a degree of protection should the energy crisis deepen in case of a harsher winter in 2023.

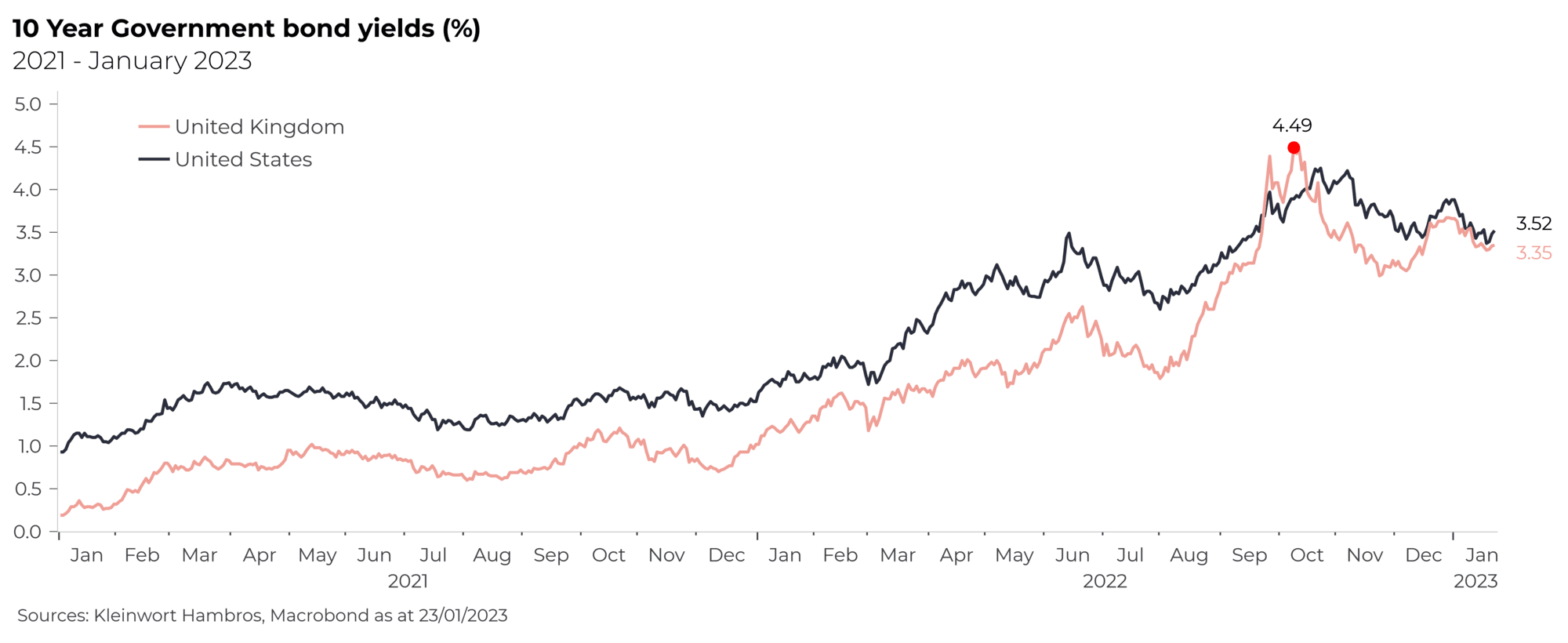

The Fed’s response to the highest-running inflation in four decades brought about the most significant bond bear market in a century. Nonetheless, US government debt remains the safe haven bellwether. Yields on 10-year treasuries have begun to stabilise just below 4% - their highest level since the Great Financial Crisis of 2008, but below average by historical standards. Prices on credit default swaps (CDS), an indicator of creditors’ ability to repay loans, on US government debt have retracted from their 2022 highs, indicating that

there is little doubt that Treasury will honour their obligations despite higher costs and a deteriorating economic backdrop.

Surging yields and plummeting bond prices may create a vicious circle of forced sellers and global bond markets, contingent on the US bellwether, plunge.

The UK gilt rout resulting from Liz Truss disastrous “mini budget” in September serves as a stark reminder of the hidden complexities of “risk-free” government bond markets in 2022. After decades of abundant liquidity, borrowers are starting to reckon with a new reality of quantitative tightening: a delicate process easily derailed by otherwise mundane trigger events. A situation similar to that in the UK is not unthinkable for the US. The $24tn Treasury market has begun to show strains given the Fed’s balance sheet runoff, and fixed income traders have grown increasingly

cautious following the uncharacteristically high levels of volatility seen over the past year, limiting deal flow. A trigger event – say political gridlock causing a delay in the authorisation of a new debt ceiling; it took the current Speaker of the House 15 attempts to get elected – could induce a UK-style selling spiral and, if left uncontained, expand to a wider US Treasury meltdown.

Treasuries’ status as the benchmark global risk-free investment makes a rout in the US bond market much more contagious than the one that occurred in the UK. Surging yields and plummeting bond prices may create a vicious circle of forced sellers and global bond markets, contingent on the US bellwether, plunge. Risk assets sell off, led by a 30% drop in US equities. The currently prevailing dollar strength dissipates, and gold emerges as ultimate safe haven, surpassing $2,200 per troy ounce.

While we continue to hold significant exposure to government bonds, we have abandoned the asset class as primary hedge to risk assets years ago, adding cash, hedge funds, gold, and other assets to “diversify our diversifiers”. Our underweight to equities, specifically to US equities that feature higher valuations than their peers, should contain some of the worst outfall in risk assets. We have also continually reduced our dollar exposure, taking advantage of the strongest greenback of the past two decades, and shortened the duration of our government bond positioning, both limiting potential vulnerability resulting from US treasury distress.

The past twelve months have been gruelling for institutional and retail investors alike. Persistent inflation, hawkish central banks, and radical uncertainty stemming from geopolitical escalations have left a mark on investor sentiment, which has reached its lowest level since the Great Financial Crisis in many developed markets. The outlook for 2023 remains murky as economic growth continues to dip and inflation – though stagnating – continues to erode consumer spending power. Central banks have not shown any real signs of pivoting, and the full effect of aggregate monetary tightening action to date has yet to feed through to corporate earnings. In short, investor sentiment is expected to remain sluggish well into the first half of 2023.

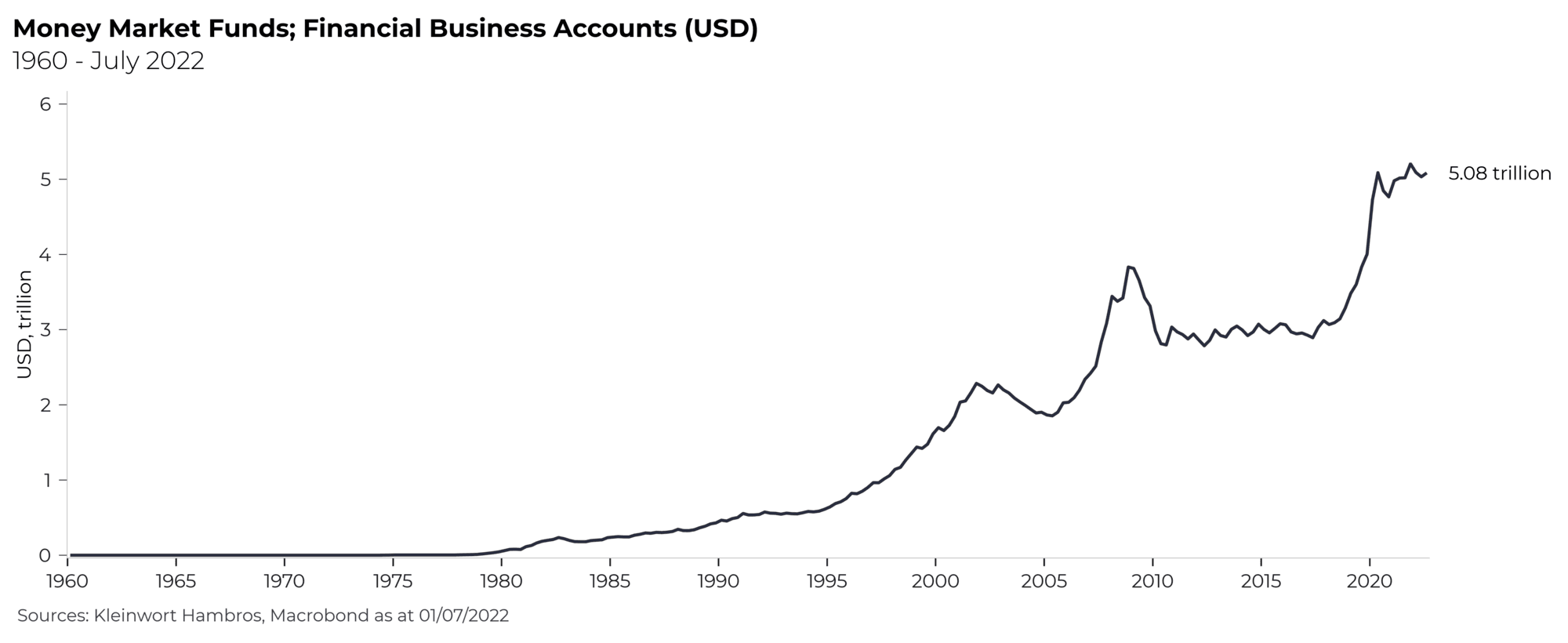

While consumer finances have come under pressure amidst persistently high inflation, monetary and fiscal expansion throughout the pandemic left balance sheets robust with much cash remaining on the side lines: an estimated $5.1 trillion is currently parked in money market funds, waiting to be deployed. Closing out 2022 with encouraging signs from inflation data combined with the famed FOMO (fear of missing out), investors become more optimistic and begin taking advantage of attractive valuations coming into the new year.

In addition to our equity exposure, our real assets fund and credit exposures are well positioned to take advantage of a recovery in investor sentiment.

From equities to bonds to crypto currencies: coming out of 2022 most asset classes appear to be valued much more attractively compared to recent history. A bout of bullish sentiment could fuel a broad rally in risk and safe haven assets alike: global equities could rally 20%, bonds 10%, and more speculative assets such as Bitcoin could double in value. On the flip side, gold prices would slump amidst risk-on sentiment, and short-term yields rise as liquidity funds dump stock to meet obligations.

Calling the bottom of a bear market is notoriously difficult, and excessively conservative market participants may lose out on significant gains by waiting for bull markets to prove themselves before re-gaining exposure. While our overall positioning is one of cautiousness – we prefer a slight underweight to equities and a large stable of diversifiers – we are maintaining significant exposure to risk assets to take advantage of any potential – or surprising – upside. In addition to our equity exposure, our real assets fund and credit exposures are well positioned to take advantage of a recovery in investor sentiment. Further, we have been retaining dry powder in the form of cash that can be deployed swiftly should we judge the return of positive momentum to be sustainable in the medium term.

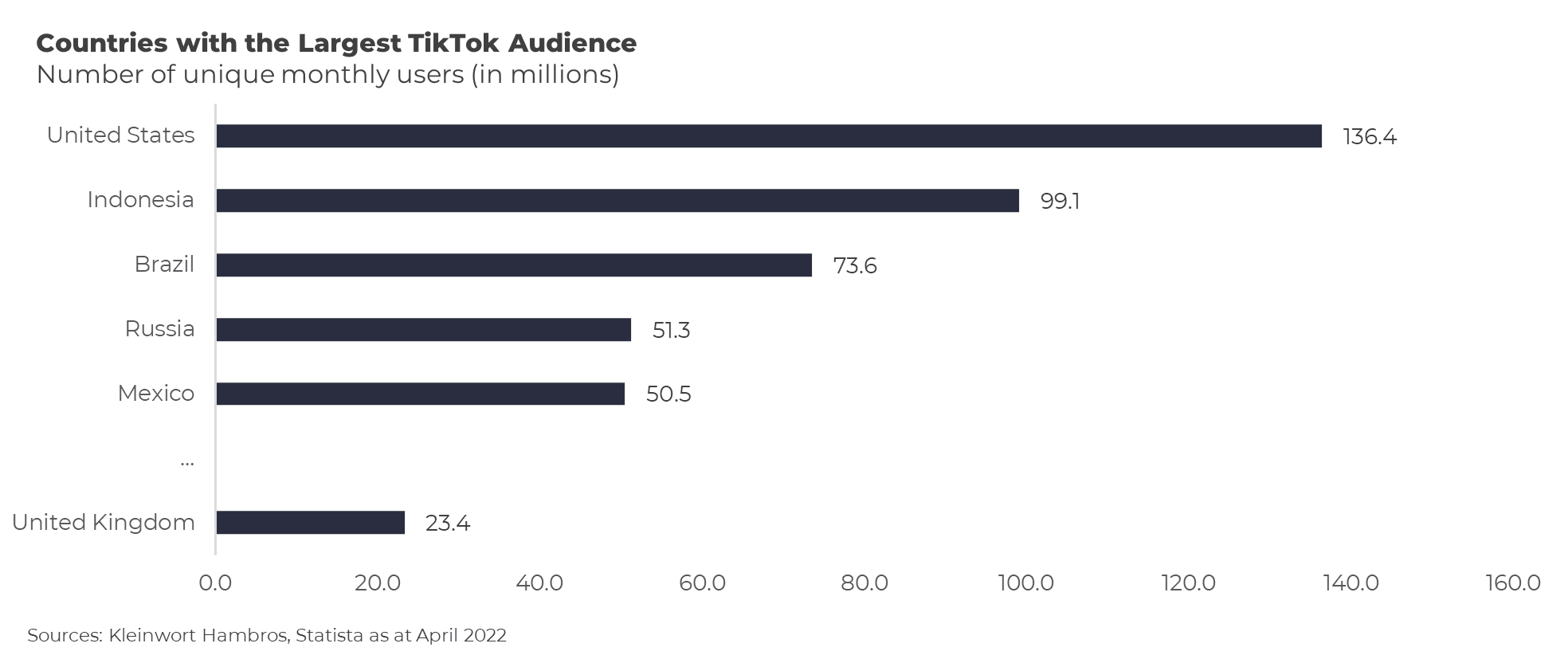

Many are likely aware of the Chinese telecommunications company Huawei. Their involvement in western 5G telecommunications was blocked on the grounds of security, their products ripped out of existing networks. The fear was it could give the Chinese government the ability to knock out or seriously degrade the western communications systems. However, there is another major channel for potential Chinese access – widespread enough the US Congress is debating a ban and already barred from US government phones – TikTok. TikTok has been downloaded over 3billion times, has 1.5 billion active users and is now the world’s 6th most popular social media product globally. In the US alone there are over 100 million users. Few are overly concerned about the widespread TikTok footprint.

Our proprietary Tail Risk Protection Note is designed specifically to take advantage of spikes in systemic volatility in financial markets.

After media clamouring and government debates Huawei now sits outside the western communications framework after numerous bans and restrictions, its projected earnings suffered significantly. The US congress is now looking at TikTok, but the current fear it poses any risk is generally minimal. From an investment view, TikTok is of little significance, but imagine if TikTok was used as a channel for the Chinese to download disruptive malware into western communications networks, something no one seems to be considering?

The US Congress is concerned about US data leakage and the possibility the Chinese could monitor the locations of US persons. Some form of malware that disrupts or cuts off access via our global communications network is unlikely, but its outfall exceptionally damaging. A US-led ban of the app would first and foremost hit technology stocks as investors mull the impact of more stringent regulation of the sector. Companies exposed to both economies, either for production or sales – or even dual-listings - would bear the brunt of the damage, slumping 20%. More generally, global equities would react poorly to the likely escalation in US-China trade relations and the VIX, a measure of uncertainty in stock markets, would spike.

Compared to a complete market meltdown resulting from a widespread & devastating malware attack, the impact of protective regulation would be relatively mundane. Over the past 24 months we have gradually reduced our exposure to the high-growth technology sectors that harbour those companies that would suffer most from additional regulation. Our proprietary Tail Risk Protection Note is designed specifically to take advantage of spikes in systemic volatility in financial markets, which an escalation in the trade war – or, absit omen, a global malware attack - would almost certainly stoke. Finally, a short-term slump in equity markets could provide attractive opportunities to deploy some of the cash we have been keeping as dry powder for such occasions.

Sources: Kleinwort Hambros, Statista as at April 2022